Structured settlements expert John Darer reviews the latest structured settlements and settlement planning information and news, and provides expert opinion and highly regarded commentary. that is spicy, Informative, irreverent and effective for over 20 years.

The STRUCTURED SETTLEMENTS 4REAL® Blog is a highly regarded source for structured settlement news, information, and commentary, led by structured settlement and settlement planning subect mater expert John Darer CLU ChFC MSSC CeFT RSP CLTC. With two decades of operation, the blog and 4structures.com are recognized as comprehensive resources, offering detailed guides and specialized insights. Established in 2005, the blog caters to a broad audience, including legal professionals, injured individuals, families, and various stakeholders, providing reviews and opinions on settlement planning. John Darer, President of 4structures.com LLC, is a seasoned structured settlement expert with over 40 years of financial services experience and 31 years specializing in structured settlements. Based in Stamford, CT, he is a Certified Financial Transitionist and Registered Settlement Planner, holding insurance licenses in 45 states and the District of Columbia. John Darer is dedicated to transparency and advocacy, he emphasizes the importance of engaging trained and licensed professionals for settlement planning, offering valuable insights through his investigative journalism and professional commentary.

You saw the banner: “Turn your future payments into Bitcoin today!” It’s loud, urgent, and built to make you click before you think. Selling a structured settlement to buy crypto isn’t a shortcut to wealth — it’s a legal sale of guaranteed income followed by a high‑risk investment. Read this before you answer any ad.

The legal reality in plain language

You cannot convert a structured settlement directly into Bitcoin or other cryptocurrency.

The only lawful path is to agree to sell your future payments to a factoring company, which requires a judge’s approval, receive a discounted lump sum, and then use that cash however you choose.

That court step exists because the system recognizes the risk of predatory deals. If an ad suggests otherwise, it’s lying by omission.

The math they don’t show

Those flashy ads never show the discount rate. When you sell, you’re selling future dollars for less today. That haircut can be large — sometimes 20–60 percent or more depending on the buyer and your payment schedule. Then you take that reduced amount and put it into crypto, an asset class known for extreme volatility. You’re trading certainty for speculation, and the numbers rarely add up in the seller’s favor.

KEY STAT

The Standard Deviation for Bitcoin over 15 years is over 180%! That’s alot of volatility. Do you see yourself as a pinball in an arcade game, ” feeling all the bumpers”?

How aggressive advertising works against you

Marketers use urgency, social proof, and fear to short‑circuit decision making. Ads promise “instant cash” and show smiling people with big gains. They target people who need money now — the exact people least able to absorb a bad outcome. If an ad pressures you to act immediately, that’s the point: panic sells. Legitimate financial decisions don’t require clicking a banner at midnight.

“Aggressive ads sell urgency. The real cost is the future income you’ll never get back.”

The real risks after the sale

You lose guaranteed income. That steady payment schedule may be the backbone of your budget.

You face crypto volatility. Prices can swing wildly; gains are never guaranteed.

You invite more pitches. Once you have a lump sum, you’ll be targeted by “investment managers,” high‑fee funds, and scams.

You may not get a fair deal. Some buyers use complex fee structures and opaque math to justify low offers. .

What to do instead

Ignore urgent ads. If it feels rushed, step away.

Get multiple written quotes. Compare discount rates and fees.

Talk to an independent attorney and financial advisor. Court approval is required; get help understanding whether a sale is in your best interest.

Consider partial sales or safer investments. You don’t have to bet everything to get liquidity.

Your structured settlement is future security, not ad bait

Aggressive advertising is designed to make you trade long‑term stability for short‑term drama. Before you click “sell,” do the math, get counsel, and remember: urgency in an ad is a sales tactic, not financial advice.

“After a disappointing end to 2025, major cryptocurrencies have languished to start the new year. Bitcoin has shed roughly one-third of its value since hitting a record high in October, including a 4.2% drop in January. Ether has slid more than 40% from last summer’s all-time highs”.

Crypto market expert Crypto Rover has warned of an 80% chance of a US government shutdown by January 31, 2026, marking a significant increase from the previous day’s estimate of 10-15%.

The potential shutdown poses a serious liquidity risk to the crypto sector. A shutdown would likely lead the US Treasury to rebuild its Treasury General Account, effectively withdrawing cash from financial markets and reducing liquidity.

This could exacerbate existing market vulnerabilities, as liquidity conditions are already strained and investor confidence remains fragile.Analysts caution that a liquidity drain could lead to significant declines in digital asset prices.

In Flatirons Bank v. Eastern Point Trust Company (Case No. 2:25-cv-00222-KHR), Judge Kelly H. Rankin GRANTED Defendant EPTC’s Motion to Dismiss on January 27, 2026. Flatirons Bank (a Colorado entity) alleged that EPTC (a U.S. Virgin Islands/Virginia entity) interfered with Flatirons’ contracts with Wyoming municipalities through pre-litigation cease-and-desist letters.

The Court dismissed the Flatirons Bank complaint without prejudice, primarily for lack of personal jurisdiction and EPTC’s immunity under the Petition Clause—deficiencies the Order noted were evident from the outset due to Flatirons’ failure to plead facts establishing forum targeting or the applicability of the “sham petition” exception.

The Order also sharply criticized Flatirons’ counsel for submitting pleadings that were legally deficient, factually inconsistent, and based on misrepresented case law.

Supplemental Material Deficiencies in Facts and Pleadings

The Court identified significant flaws in how Flatirons Bank constructed its complaint and legal arguments, reflecting that the basis for filing in Wyoming was flawed from the beginning in light of the Court’s jurisdictional and Petition Clause rulings. The dismissal was driven by Flatirons’ failure to plead facts supporting personal jurisdiction and the “sham petition” exception, and by the Court’s finding that Flatirons’ briefing contained “blatant misstatements of law.”

1. Factual Deficiencies in Pleading the “Sham Petition” Exception

Flatirons attempted to overcome EPTC’s Petition Clause immunity by arguing that EPTC’s cease-and-desist letters were “sham petitions.” The Court found this allegation materially deficient because:

Failure to Allege Objective Baselessness: The “sham” exception requires allegations supporting that the challenged petitioning activity was objectively baseless. The Court found Flatirons “included no allegations adequately refuting the objective reasonableness of EPTC’s actions.”

Contradictory Admissions: Flatirons’ own pleadings undermined its argument. The complaint acknowledged EPTC’s underlying claims regarding stolen IP and infringement. The Court noted that because Flatirons “acknowledges EPTC’s claims of infringement and theft,” the complaint actually demonstrated that EPTC had an objectively reasonable basis to send the letters.

Irrelevant Subjective Intent: Flatirons focused entirely on EPTC’s subjective intent (to harm a competitor), which the Court ruled was irrelevant because Flatirons failed the first step of proving the actions were objectively baseless.

2. Legal Deficiencies in Pleading Personal Jurisdiction

The Court found Flatirons’ jurisdictional allegations insufficient to satisfy Due Process:

Concession of Arguments: Flatirons failed to argue that EPTC’s online publications established jurisdiction in its pleadings, which the Court treated as a concession that those facts were inadequate.

Misalignment of Injury and Forum: Flatirons argued that EPTC targeted Wyoming, but the facts pleaded showed the alleged injury (economic loss) occurred in Colorado, where Flatirons is based. The Court ruled that Flatirons failed to plead facts showing EPTC targeted Wyoming itself, rather than a plaintiff who happened to have contracts there.

Professional Deficiencies in Citation and Argument The Court explicitly reprimanded Flatirons for pleadings that lacked candor: Fabricated Legal Holdings: Flatirons cited Scott v. Hern for a holding regarding a “sham exception” that the case did not contain. Misrepresentation of Outcomes: Flatirons cited CSMN Investments as a case where dismissal was reversed, when in reality, the Tenth Circuit affirmed the dismissal . The Court labeled these as “blatant misstatements of law” that cast doubt on counsel’s diligence.

The Court delivered exceptionally strong admonitions concerning the conduct of Flatirons’ legal counsel.

On False and Misleading Citations:

Pleadings containing blatant misstatements of law are unacceptable, not only hampering judicial efficiency but also casting doubt on the pleading attorneys’ diligence and candor to the court.”

On Procedural Failures (Amendment):

The Court denied Flatirons’ request to amend the complaint because it was made as a “naked request” within a response brief rather than a formal motion. The Court stated, “We have long held that bare requests for leave to amend do not rise to the status of a motion”.

Wyoming Ruling on Validity of “Browser Wrap”Forum SelectionClause

Flatirons next argues “[l]itigating the claims in the Complaint where the municipalities, evidence, and witnesses are located promotes judicial efficiency.” [ECF No. 18, at 20]. EPTC contends litigating in Virginia would create the most efficient forum “because most witnesses and evidence related to the validity of the underlying declaratory judgement claims are located there.” [ECF No. 15, at 16]. EPTC also points to litigation in the Eastern District of Michigan acknowledging the validity of its browser wrap forum selection clause and claims acting in accordance with the clause would further judicial efficiency by preventing duplicative litigation. Id. (citing Pitt, McGehee, Palmer, Bonmani & Rivers, P.C. v. E. Point Tr. Co., No. 23-CV-10166, 2023 WL 7924705 (E.D. Mich.igan)

I reached out to Flatirons Bank for comment on Judge Rankin’s decision, on January 28, 2026. The bank’s response, provided through Chanel McDowell, Vice President of Marketing and Client Experience, was:

“Flatirons Bank is dissatisfied with the Court’s ruling on personal jurisdiction; however, the lawsuit was dismissed without prejudice, permitting the refiling of the lawsuit. Consequently, Flatirons Bank will continue to address this matter through the court system.”

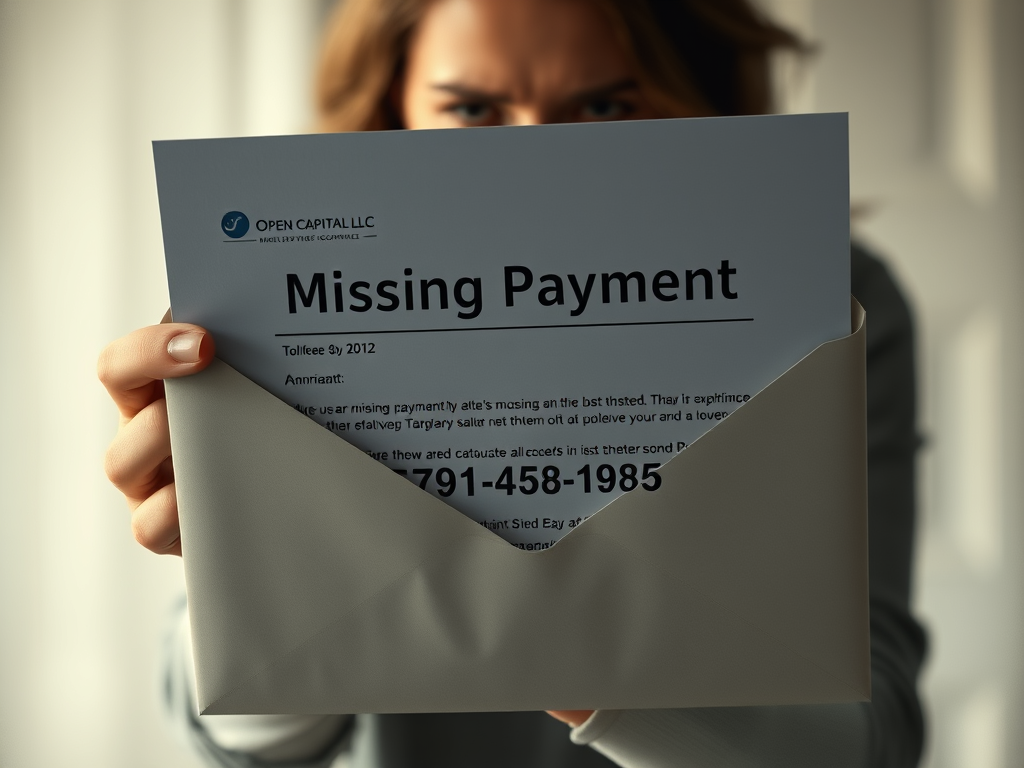

Structured settlement annuitants may be peppered with phone calls and mailers from companies seeking to buy their payments for pennies on the dollar. But the line between the truth and BS is not so fine when it comes to how vulnerable annuitants have been solicited.

Mail Solicitation into Pennsylvania by Open Capital LLC

The following in an excerpt of a mail soliciation into the State of Pennsylvania by Open Capital, LLC

“It has come to our attention that we may have an invalid address on file for your household. We’ve been trying to send you a check that was recently made available for the restructuring of your structured settlement payments.

The check has been returned to our Payment Services Department, We ask that you call an dverify your address so we can resend your check”..

The letter bears a toll free number for its “Payment Services Department” at 888-705-0870. A call to the number reaches an automatic attendant requesting that the caller leave a message.to get a call back.

Who is Open Capital, LLC

Open Capital LLC Miami, FL – filing information . Managing Member is Albert Mendez Bonita Lakes in Miami Florida Established January 24, 2013 Source: Florida Secretary of State (sunbiz.org)

Various court filings located on the internet show that this entity has been represented in structured settlement transfers by the Executive Director and General Counsel of the National Association of Settlement Purchasers.

Who is located at 3625 West Broward Blvd 2nd Floor Ft. Lauderdale, FL 33312? This address appears in a letter in the Court documents

New York Life issues structured settlement annuities through New York Life Insurance Company, oldest living life insurance company that currently issues structured settlements

Mutual of Omaha issues structured settlement annuities through United of Omaha Life insurance Company

Pacific Life issues structured settlement annuities through Pacific Life Insurance Company in all states execept New York, where Pacific Life & Annuity Company is the structured settlement annuity issuer.

Prudential issues structured settlement annuities through The Prudential Insurance Company of America

The Corebridge family includes structured settlement annuity issuers American General Life Insurance Company and United States LIfe Insurance Company in the City of New York

Special mentions for 2026

Most trustworthy: Corebridge

Most likely to be recommended to others: Mutual of Omaha

That tagline is a compliance nightmare wrapped in a sales cliché. It fails on every dimension that matters in the structured‑settlement world—truthfulness, suitability, regulatory defensibility, and basic credibility.

1. “Guaranteed” is a prohibited word in most financial‑product advertising

Regulators (state insurance departments, NAIC model regs, FTC, SEC) treat guarantee as a trigger word unless the guarantee is backed by the full faith and credit of the insurer and explicitly described.

MJ Settlements is not an insurer and as I ‘ve previously covered in other blog posts, they sell receivables to investors. They cannot guarantee anything.

Using the word implies a level of certainty and backing that does not exist.

2. “OutPerform” is an unsubstantiated performance claim

Outperform what?

The S&P 500?

Treasuries?

CDs?

Other structured settlement factoring companies?

Life‑contingent annuities?

Without a benchmark, timeframe, risk disclosure, or methodology, the claim is inherently deceptive.

3. Structured settlement receivables are not structured settlement annuities(SSA)

They are illiquid, non‑standardized, non‑transferable payment streams with credit risk tied to the issuing insurer

They do not have market‑based performance.

They cannot “outperform” in the way an investment can.

4. It misleads consumers about riskwith the type of investment

Servicing risk ( see for example, SuttonPark Nightmare) Todd Lesk LinkedIn 1/23/2026 “Some portions move quickly. Others are split, resized, or added based on investor demand” <——-PAYMENT SERVICING NEEDED to administer.

Documentation risk

Transfer‑order validity risk (see for example, Wall v Altium case, Zachary Barber case. Also see Jeffrey Barber v. Bruce Stanko, et al., 2021 PA Super 97, 2021 WL 1940513 (Pa. Super. Ct. May 14, 2021) (Appeals of Pinnacle Capital, LLC, Sempra Finance, LLC, Habitus Funding and Michael J. Pickett); Zachary Barber v. Bruce Stanko, et al., 2021 PA Super 96, 2021 WL 1940516 (Pa. Super. Ct. May 14, 2021) (Appeal of Sempra Finance, LLC).

Calling them “guaranteed” masks these risks.

5. It invites regulatory scrutiny

A regulator looking at that tagline would immediately ask:

What is guaranteed?

Who is guaranteeing it?

What data supports the claim of outperformance?

Where are the disclosures?

Why is a marketing firm, with CEO permanently barred from FINRA making investment‑style promises?

They would not like the answers.

🧭 What the tagline really communicates

To a sophisticated reader, it signals:

Unsophisticated marketing

A lack of understanding of financial‑product compliance

A willingness to mislead yield‑chasing retail buyers

A red flag about the firm’s culture and ethics

It’s the kind of statement that reveals more about the company than intended, even before reviewing the FINRA record, which resembles a target at a shooting range with direct hits to center mass. There remain outstanding claims. Prior to identifying Todd Lesk’s LinkedIn profile on January 17, 2026, he was still promoting his former FINRA licenses more than two years after consenting to be permanently barred.

🛠 If you wanted to rewrite it into something more defensible…

For contrast:

“Designed for predictable income streams.”

“Built on fixed, court‑ordered payments.”

“Focused on stability, not speculation.”

Those are boring, but they’re compliant. “Guaranteed to OutPerform” is neither.

⚠️ Why “Guaranteed to OutPerform” Is a Triple‑Violation Tagline

1. The word “Guaranteed” is legally radioactive

In financial‑product advertising, guarantee is one of the most tightly restricted words in the entire regulatory lexicon.

Why it’s a problem:

Only insurers can guarantee payments, and only to the extent of their contractual obligations.

MJ Settlements is not an insurer. They cannot guarantee anything.

Using “guaranteed” implies:

A financial backstop

A credit guarantee

A performance guarantee

A regulatory guarantee None of which exist.

Regulatory bodies that would object:

State insurance departments

NAIC Model Regulation on Advertising

FTC deceptive advertising rules

State UDAP statutes

Attorneys General

Plaintiff attorneys in consumer actions

This single word alone is enough to trigger an investigation.

2. “OutPerform” is an unsubstantiated performance claim

To claim outperformance, you need:

A benchmark

A time horizon

A risk‑adjusted methodology

Historical data

Disclosure of assumptions

MJ Settlements provides none of these.

Outperform what?

The S&P 500?

Treasury yields?

CDs?

Other factoring companies?

Life insurance general accounts?

Inflation?

Bank savings rates?

Without a benchmark, “outperform” is inherently deceptive.

And structured settlement receivables cannot “perform” in the investment sense

They are:

Illiquid

Non‑marketable

Non‑standardized

Dependent on insurer creditworthiness

Dependent on court‑ordered payment streams

They do not have “performance.” They have fixed payments.

Calling them “outperformance vehicles” is like calling a refrigerator “faster than a Ferrari.”

3. The combination of “Guaranteed” + “OutPerform” is a regulatory red flag

This pairing is the exact type of language regulators cite in enforcement actions.

It implies:

Zero risk

Superior returns

Certainty of advantage

Investment‑like performance

A promise of results

This is the kind of language that gets:

Fines

Cease‑and‑desist orders

Mandatory corrective advertising

Class‑action exposure

Referral to state AGs

It’s the financial‑advertising equivalent of yelling “FIRE” in a crowded theater.

4. It misleads consumers about the nature of the product

Structured settlement receivables are:

Not investments

Not securities

Not guaranteed by the government

Not guaranteed by insurers beyond their contractual obligations

Not guaranteed by MJ Settlements

Not risk‑free

Yet the tagline implies:

Safety

Superiority

Predictability

Market‑beating returns

This is the opposite of transparent consumer communication.

5. It signals a lack of sophistication and credibility

To a professional audience, the tagline communicates:

Unsophisticated marketing

A misunderstanding of financial compliance

A willingness to mislead yield‑hungry retail buyers

A disregard for regulatory norms

A red flag about the firm’s culture

It’s the kind of line that makes serious professionals walk away.

Why “Guaranteed to OutPerform” Is a UDAP Time Bomb Waiting to Explode

Every few years, a marketing slogan comes along that perfectly captures what regulators warn against, what UDAP statutes prohibit, and what plaintiff attorneys dream of finding in discovery. MJ Settlements’ tagline — “Guaranteed to OutPerform” — is one of those slogans.

It’s bold. It’s reckless. And under consumer‑protection law, it’s the kind of statement that can turn a marketing campaign into a liability event.

Below is a breakdown of why this phrase is legally indefensible and why it should concern anyone who cares about transparency in the structured settlement marketplace.

1. UDAP 101: Why This Phrase Is Deceptive on Its Face

UDAP (Unfair and Deceptive Acts and Practices) statutes exist to stop companies from misleading consumers. They apply to all financial products — including structured settlement payment rights and receivables.

A statement is deceptive if it is:

Likely to mislead a reasonable consumer

Material to the consumer’s decision

Unsupported by evidence

“Guaranteed to OutPerform” checks all three boxes.

A. “Guaranteed” is a prohibited implication of certainty

Consumers hear “guaranteed” and reasonably assume:

Zero risk

A financially capable guarantor

A legally enforceable promise

MJ Settlements is not an insurer. It cannot guarantee anything — not payments, not yields, not performance.

B. “OutPerform” is an unsubstantiated performance claim

Outperform what?

The S&P 500?

Treasuries?

CDs?

Other factoring companies?

Inflation?

Structured settlement receivables do not have performance in the investment sense. They have fixed payments and credit risk. There is no benchmark, no market index, and no performance curve.

Claiming outperformance is inherently deceptive.

C. The combination is explosive

“Guaranteed” + “OutPerform” is exactly the kind of pairing UDAP statutes were written to prevent — a false promise of superior, risk‑free returns.

2. Why the Tagline Is Also “Unfair” Under UDAP

Unfairness under UDAP requires:

Substantial consumer injury

Not reasonably avoidable

No countervailing benefit

This tagline meets all three.

Substantial injury

Consumers may:

Overpay for payment streams

Misunderstand credit risk

Believe returns are guaranteed

Forego safer alternatives

Not reasonably avoidable

Consumers cannot:

Evaluate insurer solvency

Assess discount‑rate fairness

Understand transfer‑order validity

Compare illiquid receivables to market investments

No benefit

There is no legitimate consumer benefit to a false performance guarantee.

This is the definition of an unfair practice.

3. Why the Tagline Is “Abusive” Under UDAAP

Under Dodd‑Frank, a practice is abusive if it:

Materially interferes with consumer understanding, or

Takes unreasonable advantage of consumer vulnerabilities

This tagline does both.

Material interference

It obscures:

Risk

Liquidity limitations

Credit exposure

The true nature of the product

Unreasonable advantage

It exploits:

Information asymmetry

Consumer unfamiliarity with structured settlement receivables

The desire for “safe high yield” products

This is classic UDAAP territory.

4. How a Plaintiff Attorney Would Use This Tagline Against the Company

A plaintiff attorney would treat “Guaranteed to OutPerform” as a gift.

They would argue:

A. The guarantee was false the moment it was made

This supports:

Negligent misrepresentation

Intentional misrepresentation

Breach of warranty

False advertising

B. The performance claim was unsubstantiated

They would demand:

The benchmark

The methodology

The historical data

The risk disclosures

MJ Settlements cannot produce any of these.

C. The consumer relied on the misrepresentation

Reliance is easy to prove when the misrepresentation is the tagline.

D. Damages flow naturally

Overpayment

Loss of liquidity

Lost opportunity cost

Emotional distress

Punitive damages

Punitive damages become likely because the conduct is bold, absolute, and reckless.

5. Why This Matters for the Structured Settlement Industry

The structured settlement industry has spent decades building credibility around:

Safety

Predictability

Suitability

Transparency

A tagline like “Guaranteed to OutPerform” undermines all of that. It invites regulators to scrutinize the entire marketplace. It misleads consumers at their most financially vulnerable moments. And it signals a culture that prioritizes yield‑chasing over ethics.

This is not harmless puffery. It’s a UDAP violation waiting to happen.

Bottom Line

“Guaranteed to OutPerform” is not just bad marketing — it’s a legal hazard, a regulatory trigger, and a consumer‑protection failure. It misrepresents the nature of the product, overstates benefits, conceals risks, and violates every major UDAP/UDAAP standard.

For an industry built on trust, this kind of language isn’t just sloppy. It’s dangerous.

Todd Michael Lesk, the CEO of MJ Settlements, consented to be PERMANENTLY BARRED from FINRA on October 6, 2023 (Source: FINRA and IAPD which states “FINRA has barred this individual from acting as a broker or otherwise associating with a broker-dealer firm”

Todd Lesk is Permanently Barred From FINRA in ANY Capacity

Despite Lesk’s acceptance of his being permanently barred from FINRA per above, on January 17, 2026 the following was an observed (and preserved here for reference purposes) excerpt of Todd Lesk’s Linkedin, under which Lesk lists “Licenses and Certifications” and lists as “LICENSED” for FINRA Series 24, Series 6 and Series 7 and Series 2-15 for Florida Department of Insurance and Financial Services..

Lesk makes regular use of LinkedInas does the company of which he is CEOwith the “Deal of the Day-Starter Investment Opportunity!“, as an example

Regular postings on social media list Deal of the Day — Starter Investment Opportunity!

Structured settlement receivables investment solicitations are placed in the “shop window” without using the accurate term receivables, which are not annuities or insurance products.

To Avoid Any Confusionabout Lesk’s Licenses and Certificationsfrom His Ongoing LinkedIn Display

Todd Michael Lesk’s former Series 24 license (and any other FINRA securities licenses he previously held). has not been valid since his FINRA barring.. Here’s the breakdown:

FINRA’s permanent bar (imposed in October 2023) prohibits him from associating with any FINRA member firm in ANY capacity. This includes supervisory/principal roles that require the Series 24 (General Securities Principal Qualification).

A permanent bar from FINRA effectively cancels or renders inactive all associated representative and principal qualifications/licenses under FINRA jurisdiction. The Series 24 is a principal-level qualification that only remains active/valid while the individual is properly registered and associated with a FINRA member firm (and complies with ongoing requirements like continuing education).

Once barred, an individual cannot re-register or reactivate those licenses without FINRA approval (which is extremely rare and typically not granted for statutory disqualification-level bars like non-cooperation).

Watchdog Barks, Todd Lesk Harks

I know that Todd Lesk reads this blog, and less than a week after I posted this obervation, The subject misrepresenations on Todd Lesk’s LinkedIn have been removed. The following was captured on January 21, 2026

What does THAT have to do with a Whale-y good, ethical structured settlement annuity issuer from The Left Coast and its Index Linked Annuity Payment Adjustment Rider?

The Teddy Bears Picnic

Goldilocks joined the bears down in the woods one day later. They sure had a big surprise when they discovered an interesting, sophisticated watchdog drinking from a glass of milk with something witty to say on the subject.

Next Episode…The Bear Market Rally

I can “barely believe” that any structured settlement consultant, not selling short would focus on the “porridge being just right”.after the taste tester burgled, ate the food, scent marked the furniture when the symbolism of the bear is a market going down.

Is a structured settlement annuity ours, yours, or theirs?

The image was captured on January 8, 2026. It is part of an online ad from a structured settlement factoring company. This ad is awkwardly placed in a news story about a fatal shooting in Minneapolis, Minnesota on January 7, 2026.

The tag line “Cash Our Your Annuity” presents a easily rebuttable presumption:

Key Points

Structured settlement annuities are not owned by structured settlement payees.

Structured settlement payees can’t sell what they do not own.

Structured settlement payees can sell structured settlement payment rights. The sale must follow IRC 5891 and applicable Structured Settlement Protection Acts.

Investors in structured settlement receivables do not own structured settlement annuities,

” Secondary Market Annuities” are not annuityies at all. They are receivables.

Egan-Jones is registered with the U.S. Securities and Exchange Commission as a Nationally Recognized Statistical Rating Organization (NRSRO) for certain asset classes (Egan-Jones is NOT registered as an NRSRO in respect of issuers of asset-backed securities or issuers of government, municipal or foreign government securities), and certified by both the European Securities and Markets Authority and UK Financial Conduct Authority. Source: Egan-Jones

NRSROs and Insurers, including Structured Settlement Annuity Issuers

For insurers, having a higher BBB rating instead of a BB can significantly cut capital requirements and increase returns. Ratings really do matter.

A. M. Best.

Standard & Poors

Moodys

Fitch

Egan-Jones

KBRA

The credit ratings potentially affect access to capital and the rates charged for the capital.

Consider it similar to the scenario where an individual with an 800 personal credit score applies for a credit card, car loan, or mortgage, compared to an applicant with a 600 score on Equifax, Experian, TransUnion, or FICO, when seeking terms for a mortgage, car loan, or home remodeling loan.

Mid-year 2025 Concernssaw ” a growing list of institutional investors-including BlackRock, Carlyle and Apollo-have formally excluded Egan-Jones from their deals”-Guru Focus June 26, 2025

Some industry insiders point to ratings that are “investment-grade” on paper but feel misaligned with the actual risk.

But a now-withdrawn NAIC report highlighted that firms like Egan-Jones may be assigning grades several notches higher than expected. Meanwhile, recent blowups are testing confidence: Chicken Soup for the Soul, Crown Holdings, and other companies defaulted soon after receiving BBBs from Egan-Jones. Even so, the firm insists its methodology holds up. “Our rated obligations have typically performed better than implied,” Egan-Jones said in a recent statement. Critics remain unconvinced, especially when defaults happen within weeks.

The firm also faces pressure off the balance sheet. A 2022 SEC settlement barred founder Sean Egan from rating decisions and imposed $2 million in penalties over alleged conflicts of interest. Then in 2024, two ex-employees sued, alleging they were fired for questioning internal practices — including pressure to modify ratings. That case is still in court. Despite the noise, Egan-Jones is pushing forward. But with more scrutiny, slower growth, and mounting concerns about systemic risk, investors may need to think harder about the fine print behind those private credit labels — and who’s writing them.

A good-natured ribbing for Jovan Johnson. He is the celebrated chocolate chip cookie lover and fish taco aficionado from San Francisco. Johnson has a location on Tennessee Street. He generates leads to ‘free Willy’ (your annuity or structured settlement) for pennies on the dollar. He does this through multiple websites, like AnnuityFreedom and Paymaster.

Apparently from the above the S.S. Johnson has slipped its moorings in South Carolina and taken an unscheduled scenic cruise up the Eastern Seaboard. One expects stops in Charleston, Sumter, Columbia, and Hilton Head. The journey also include Kiawah Island, Myrtle Beach, Greenville, Spartanburg, or Aiken. There’s a little road work thrown in for good measure. After all, didn’t the captain say “make haste,” not “cut and paste”?

As you can see from the header, Willy has freely set off with his favorite snack in tow. No “cheap krills” this time—just solid, time-tested navigation tips. And remember, never forget the Toll House “Morsel Code.”