Structured settlements expert John Darer reviews the latest structured settlements and settlement planning information and news, and provides expert opinion and highly regarded commentary. that is spicy, Informative, irreverent and effective for over 20 years.

The STRUCTURED SETTLEMENTS 4REAL® Blog is a highly regarded source for structured settlement news, information, and commentary, led by structured settlement and settlement planning subect mater expert John Darer CLU ChFC MSSC CeFT RSP CLTC. With two decades of operation, the blog and 4structures.com are recognized as comprehensive resources, offering detailed guides and specialized insights. Established in 2005, the blog caters to a broad audience, including legal professionals, injured individuals, families, and various stakeholders, providing reviews and opinions on settlement planning. John Darer, President of 4structures.com LLC, is a seasoned structured settlement expert with over 40 years of financial services experience and 31 years specializing in structured settlements. Based in Stamford, CT, he is a Certified Financial Transitionist and Registered Settlement Planner, holding insurance licenses in 45 states and the District of Columbia. John Darer is dedicated to transparency and advocacy, he emphasizes the importance of engaging trained and licensed professionals for settlement planning, offering valuable insights through his investigative journalism and professional commentary.

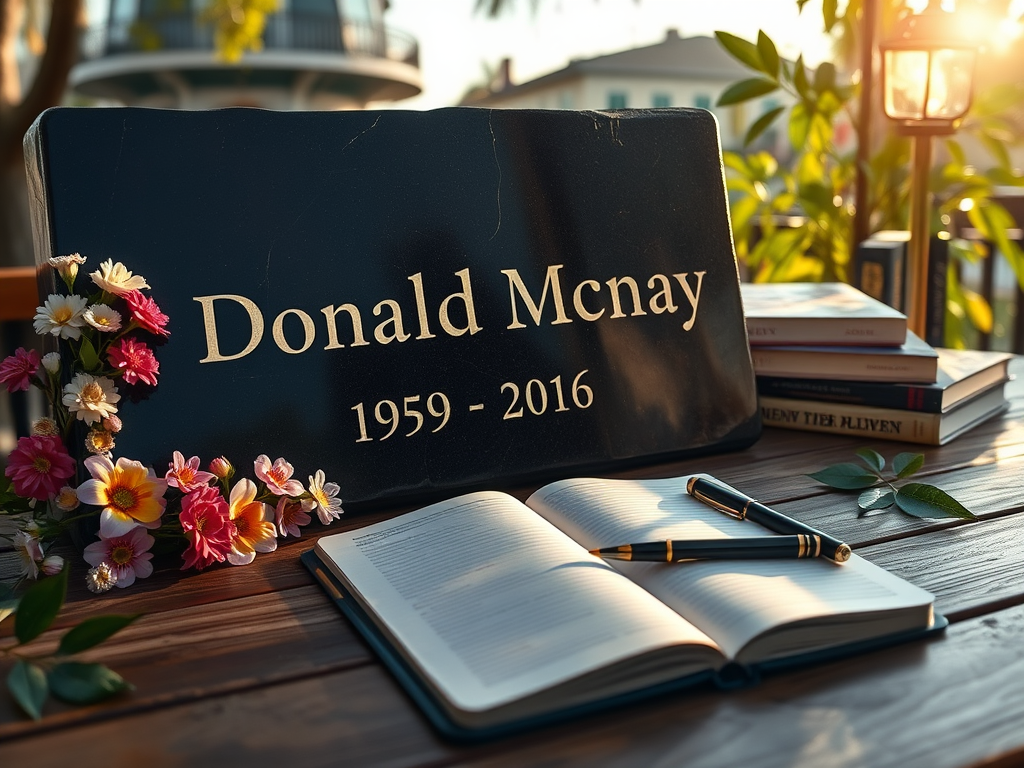

Donald “Don” Joseph McNay, beloved husband and father, best-selling author and national columnist, passed away unexpectedly May 29, 2016 at age 57 in New Orleans while visiting his wife, Dr. Karen Thomas McNay who serves there as President of Ursuline Academy. Born in Covington, Ky. Feb. 13, 1959 to parents Joseph O. McNay and Ollie O. McNay, Don was the first of three children. He attended Covington Catholic High School and Eastern Kentucky University, where he graduated with a Bachelor’s Degree in Journalism and Political Science in 1981. His rapid success led to induction into the EKU Hall of Distinguished Alumni in 1998. Don earned a Master’s Degree from Vanderbilt University, graduated with a second Master’s from the American College of Financial Services in Bryn Mawr, Pa., and went on to obtain four coveted professional designations in the financial services field.

Founded McNay Settlement Group

He founded McNay Settlement Group Inc. in 1982 where he participated in more than 1,000 mediations and became one of the nation’s leading experts in helping people who are awarded large sums — in insurance cases, from state lotteries and other situations – to structure their finances. He served on the Board of Directors for the National Structured Settlement Trade Association and the Society of Settlement Planners. He actively participated in and commented on politics, serving as Assistant Kentucky State Coordinator for Al Gore’s successful presidential primary campaign in 1988 and as Campaign Treasurer for Former Secretary of State and State Auditor Bob Babbage in his 1995 gubernatorial campaign.

Was One of the World’s Leading Authorities on How Lottery Winners Handle Their Money

As one of the world’s leading authorities on how lottery winners handle their money, Don appeared on hundreds of national and international media programs. He was a frequent guest on Comment on Kentucky, the longest running public affairs program on Kentucky Educational Television (KET) and during many KET shows covering election results.

Syndicated Columnist and Author

Don wrote a syndicated column for CNHI News Service, served as a community columnist for the Lexington Herald-Leader and regularly contributed to The Huffington Post. He wrote eight best-selling books, including his most recent book, called Brand New Man: My Weight Loss Journey, which detailed his story following bariatric surgery. He was the owner of RRP International, a publishing and digital media company based in Lexington, Ky. He won “Best Columnist” from the Kentucky Press Association in 2005, and also served as Treasurer of the National Society of Newspaper Columnists. The Lexington Jaycees named Don their Outstanding Young Lexingtonian in 1985.

He was an honorary Kentucky Colonel, and the mayor of Hazard designated him an honorary Duke of Hazard. He became a University Fellow at both EKU and the University of Kentucky, and was appointed to the Board of Directors for the EKU Foundation as a member of the Investment Committee. To his many friends and family members, Don is remembered as a passionate, loyal, generous, intelligent, larger-than-life person who deeply cared about and helped others. His many diverse interests included Cincinnati Reds baseball, CrossFit exercise, rock and roll history, public affairs and the stock market. He deeply loved his wife Karen, his children and relatives, and was fiercely loyal to those fortunate enough to call him friend. Don was preceded in death by parents Joseph McNay (1933-1993) and Ollie McNay (1939-2006) and his sister Theresa Ann McNay Francis (1969-2006). In addition to his wife Karen, he is survived by his daughters Angela Luhys and Gena Bigler, step-daughter Emily Kirby, step-sons Max and Zack Kirby, son-in-law Clay Bigler, nephew Nick McNay, half-brother Joseph John McNay, and three grandchildren: Abijah Luhys, Liam Bigler and Adelaide Bigler.

Shared Playful Banter on Music

Don and I shared our mutual interest in music. Fond memories of playful banter with Don on his song selection to promote structured settlements

A website called Secondary Annuities is pirouetting off the high dive with a fantasy ad.

First: The Misleading Claimsabout Structured Settlement Receivables

“Think of it like buying a barely-used luxury car. Same manufacturer, same reliability, same car – but at a 10-15% discount because someone else drove it off the lot first”.

“The insurance company doesn’t care who receives the payments”

“The math doesn’t change. You just get a better deal because you’re buying recycled settlement payments instead of brand-new contracts”.

What’s Being Left Out?

You’re not buying a Lambo, Bugatti or Maserati bro, even figuratively speaking.

If you were buying a “barely-used luxury car (or any car), the car would need to be inspected and certified road worthy See for example in Connecticut, Chapter 743f – Used Automobile Warranties

You’re not buying an annuity, your’e buying a receivable.

A structured settlement receivable is not an annuity

A structured settlement receivable is not an insurance product

If you buy a structured settlement receivable there is good chance it is a part of a slice and dice, A slice and dice happens when the original payee under a structured settlement sells part of a payment stream or deferred lump sum, or a receivable is chopped up in to smaller more manageable pieces to attract greater demand from potential buyers at lower price leevels

You may or may be aware that slice and dice requires a payment servicing arrangement that puts you a step removed from the annuty issuer. Now .Google “SuttonPark”, ” SuttonPark Nightmare“, “Josh Wander” and “777 Partners“. “SMA Hub” for some “light reading”

In 80% of US states you have no protection in the event of insolvency of the annuity issuer.

Annuity.org says “If you’re purchasing an annuity, make sure your check or wire transfer is made out to the life insurance company (your annuity contract is with them), not the advisor or any other individual.” ” How to Protect Yourself from Annuity Scams”, a subsection in an article titled “Annuity Scams” by Lena Muhtadi Borrelli which is listed as recently updated December 8, 2025.

So who is being targeted with a sales pitch for the ignorant? Is it you?

” Significantly, these investments are not annuities and they are not structured settlements as that term is defined in IRC section 5891(c)(1).” said Patrick Hindert, co-author of the book Structured Settlements and Periodic Payment Judgments, in “Re-cycled Structured Settlement Payment Rights” Independent Life blog September 28, 2020

It’s ironic that MJ Settlements includes the statement in a pargaraph called “Trust” Captured for reference purposes December 26, 2025.

What is Trust?

assured reliance on the character, ability, strength, or truth of someone or something (Source: Merriam Webster)

The attitude of expecting good performance from another party, whether in terms of loyalty, goodwill, truth, or promises. The importance of trust as a kind of invisible glue that binds society together is most visible when it is lost. Trust involves an element of risk, and epistemologists can have trouble categorizing it as rational, since it works best in advance, for example to motivate performance on occasions when defection may be to the advantage of the person trusted. Economically trust is precious, enabling parties to bypass the costly precautions and safeguards needed in transactions with parties whom one does not trust. Trustworthiness is a virtue, subsuming varieties such as truthfulness and fidelity. It is a general ambition of democratic politicians to be trusted whether or not they are trustworthy.(Source: Oxford English dictionary)

Is a Permanent Bar from FINRA an example of Trust?

“You can use it to indicate that something is backed up or endorsed by another thing, or that one thing acts as a foundation for another.”

The current offering sheet for MJ Settlements lists structured settlement receivables are said to be from Trans America Life. Sounds like something you get at a Pontiac dealership, with a spoiler and a Firebird painted on the hood, or perhaps something else..

Transamerica’s parent company, Aegon N.V., sold its entire block of existing, closed structured settlement annuity business in a reinsurance deal with Wilton Reassurance Company in June 2017. We’re talking 8.5 years prior to the date of this posting and the current listing for sale on MJ Settlements. Transamerica had already placed this business in “run-off” mode, meaning it stopped selling new structured settlement products in 2003, years before the 2017 sale.

What part of sold its entire block of existing, closed stuctured settlement annuty business does Todd Lesk not understand? Tranamerica has not issued stuctured settlement annuities since 2003!

Leo Govoni, the 67 year old Clearwater Florida entrepreneur and founder of the shuttered Centers for Special Needs, indicted over the disappearance of $100 million from medical trust funds has been battered and assaulted in a Florida Jail on November 23, 2025. Govoni has been jailed since being denied bail in July 2025. See Leo Govoni assaulted in Pinellas jail, moved to Hernando facility

The IRS is investigating whether Brook-Hollow Capital LLC and Brook Hollow Financial LLC may be liable for civil penalties pursuant to 26 U.S.C. § 6700 “for organizing or promoting abusive tax shelters”

The Internal Revenue Service is investigating whether Brook-Hollow Capital LLC and Brook-Hollow Financial LLC (collectively “Brook-Hollow”) may be liable for civil penalties pursuant to 26 U.S.C. § 6700 for organizing or promoting abusive tax shelters. (Second Declaration of Revenue Agent Elizabeth Walker (Doc. 24,. Ex. 1, “Second Walker Decl.”) ¶ 2). Based on the investigation to date, the IRS understands that Brook-Hollow offers deferred legal fee programs that purport to defer the receipt of a law firm’s fees, payable out of a settlement amount negotiated by the law firm on behalf of its client.

UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF OHIO WESTERN DIVISION UNITED STATES OF AMERICA, Petitioner, Case No. 1:24-mc-13 v. TATE JOHNSON, Defendant

The IRS issued summonses that seek documents and records concerning Brook Hollow’s deferred fee structures, the law firms that have participated in those structures and the related financial arrangements

On their face, these categories are reasonably calculated to shed light on how Brook-Hollow’s programs operate, how they are marketed, and how income is treated for tax purposes. The relevance standard in the summons context is broad: information is relevant if it “might throw light upon the correctness” of the return or liability under investigation. Powell, 379 U.S. at 57.

Source: Case: 1:24-mc-00013-SJD-SKB Doc #: 26 Filed: 12/11/2025 Page: 5 (footnote) and 6 of 12

” The Requested information easily meets the standard”

Respondent argues that Petitioner has not established that the Court has jurisdiction to hear this matter as the pleadings, as a whole, do not make clear that enforcement is sought against Brook Hollow Capital and Brook Hollow Financial—the parties to whom the summonses were addressed. See Parker v. Graves, 479 F.2d 335, 336 (5th Cir. 1973). However, Respondent contends that Petitioner’s pleadings largely indicate that enforcement is sought against Tate Johnson personally. Petitioner notes that the “caption of a complaint is not part of the statement of claims against any alleged defendants, but is chiefly for a court’s administrative convenience for identifying the case.” Church v. City of Cleveland, 2010 WL 4883433, at *3 (N.D. Ohio Oct. 26, 2010), report and recommendation adopted, 2010 WL 4901739 (N.D.Ohio Nov. 23, 2010). The “determination of whether a defendant is properly in the case depends upon the allegations in the body of the complaint.” Eberhard v. Old Republic Nat’l Title Ins., 2013 WL 12293449, at *5 (N.D. Ohio Sept. 13, 2013) (collecting cases).

The Petition and the accompanying declaration (and the second declaration of Revenue Agent Walker) establish that the IRS properly issued these summonses to (Tate) Johnson as President and partnership representative of Brook-Hollow, to obtain Brook Hollow’s records”

Here, the summonses themselves identify to whom the summonses are issued and what documents are sought.

The Petition, and the accompanying declaration (and the second declaration of Revenue Agent Walker) establish that the IRS properly issued these summonses to Johnson, as president and partnership representative of Brook-Hollow, to to obtain Brook Hollow’s records.

As such, Respondent’s contention in this regard is not well-taken.

What Brook Hollow Capital says on its website about the loans

A CT structured settlement seller with a brain injury lost his entire lump sum after converting it into cryptocurrency — a predictable disaster made possible by the absence of mandatory Independent Professional Advice (IPA) under Connecticut law.

The CT Structured Settlement Protection Act does not mandate Independent Professional Advice

If Independent Professional Advice was mandatory for all CT structured settlement transfers of payment rights, as it should be, the Connecticut man with an obvious brain injury would have been adequately protected

It underscores the need for transparency and proper guidance in making financial decisions involving a CT structured settlement.

CT Structured Settlement…A Bridge to Crypto is a Terrible Idea

An Unfortunate Narrative being delivered in Social Media and in press releases

I thought you might like to read the following that I wrote to increase awareness of this latest arrow being directed at structured settlement annuitants.

Earlier today, I spoke with a Prudential annuitant whom I had not met before. His speech immediately suggested that he had a brain injury.

The annuitant disclosed to me that he had informed the factoring company of his brain injury; AND

that a representative from the factoring company allegedly told him they would not include this information in the petition, as it might affect the court approval process.

I believe the original records for establishing the structure may have indicated the source of the personal physical injury.

I learned that another more prominent structured settlement factoring company declined the deal due to their independent assessment of the annuitant’s life expxectancy and concomitant likelihood of recovering their investment.

If one were to presume that the factoring company that completed the deal charged the brain injured CT resident a hefty price.

I learned from reviewing Court records that there was no Independent Professional Advice.

The annuitant with brain injury proceeded to invest in crypto and lost all his money.

The transfer was only completed in early 2025.

🧨 The Coaching Problem: When Disclosure Becomes a Liability

What makes this case even more disturbing is that the seller did disclose his brain injury — just not to the court. He told the factoring company directly. And according to his account, a representative allegedly coached him not to include that information in the petition because it might jeopardize court approval. This is the perverse chicken‑and‑egg routine at the center of too many transfers: if the seller discloses a cognitive impairment, the judge won’t approve the deal; if he doesn’t disclose it, the buyer gets the transaction through. The party with the most to gain from nondisclosure is the one controlling the paperwork. That is not consumer protection. That is a structural flaw that leaves vulnerable people exposed.

📍Why This Belongs on Connecticut Attorney General William Tong’s Radar

This is precisely the kind of conduct that should be on Connecticut Attorney General William Tong’s radar. When a factoring company allegedly coaches a cognitively impaired seller not to disclose a brain injury because disclosure might jeopardize court approval, the system isn’t protecting the individual — it’s protecting the transaction. That inversion of incentives is a consumer‑protection failure, and it falls squarely within the Attorney General’s mandate to investigate unfair, deceptive, or abusive practices affecting Connecticut residents.

Was the Member of the Connecticut Bar that represented the Transferee at the Hearing made aware of the seller’s brain injury?Why wasn’t the deal flagged by the buyer?

This happened in Connecticut, but nothing about the failure is uniquely Connecticut — the same vulnerabilities exist anywhere a cognitively impaired seller is pushed through a transfer process without real safeguards..

Unfortunately, Connecticut is among the majority of states that do not require Independent Professional Advice.

This case exposes a deeper structural flaw: the Protection Acts were designed for a different era — one without crypto, meme‑assets, or aggressive digital marketing aimed at vulnerable populations. When a cognitively impaired person can sell a lifetime income stream and immediately funnel the proceeds into a speculative asset class, the law is not merely outdated. It is failing in real time.

Mandatory IPA is not a bureaucratic burden; it is the firewall between a vulnerable seller and irreversible harm. It ensures that someone with diminished capacity is not left alone in a marketplace filled with discount buyers, opaque pricing, and seductive “cash now” narratives. Without IPA, the system relies on luck — and luck is not a consumer‑protection strategy.

What is Independent Professional Advice?

Independent Professional Advice (IPA) is the safeguard that ensures a structured‑settlement seller fully understands the financial, legal, and long‑term consequences of transferring their payment rights. It must be delivered by a qualified, independent professional — not the buyer, not the buyer’s attorney, and not anyone with a financial interest in the transaction. Proper IPA evaluates the fairness of the discount rate, the seller’s capacity, the suitability of the transfer, and the long‑term impact on medical care, public benefits, and financial stability. For a deeper explanation of how IPA is supposed to function — and why its absence was so consequential in this Connecticut case — see Independent Professional Advice (IPA) for Structured Settlement Sellers (4structures.com)

🛡️Why Connecticut Must Mandate Independent Professional Advice

Connecticut’s failure to require Independent Professional Advice (IPA) leaves cognitively impaired sellers exposed to irreversible harm, as this case makes painfully clear. A man with a documented brain injury was able to sell off his structured settlement, convert the proceeds into a high‑risk crypto position he did not understand, lose nearly everything within months, and then try—desperately—to undo what had been done. None of the safeguards that should have protected him were triggered: no capacity screening🧠, no suitability review📉, no independent professional evaluating whether he understood the transaction or the risks⚠️. Without a statutory IPA requirement, courts are left blind👁️🗨️, buyers are left unchallenged, and vulnerable residents are left to navigate a process they cannot meaningfully comprehend. Connecticut can prevent this from happening again, but only if IPA becomes mandatory.

In 2016, I noted that “while the Affordable Care Act aimed to make health insurance more affordable, “recent market developments and projected rate increases for upcoming renewals present challenges to using ACA policies as a means to mitigate damages during settlement negotiations.” Affordable Care Act Blog August 22, 2016

Less than a decade later, the political climate continues to validate my cautious assessment of the challenges of the strategy..

Claims and Litigation Management Suggested Use of ACA to Mitigate Damages in Your Personal Injury Case at Mediation

“Even before trial, the availability of insurance through the ACA may be more effectively raised in settlement discussions. Defendants should prepare multiple cost scenarios, including the annuity cost of the plaintiff’s life care plan, the annuity cost of the plaintiff’s life care plan with insurance, the annuity cost of the defendant’s life care plan, the annuity cost of the defendant’s life care plan with insurance, and the annuity cost of the plaintiff’s life care plan utilizing the proper paid rates for the medical goods and services identified in the life care plan. Additional savings can be realized on these annuitized cost projections by utilizing medical underwriting. The structured settlement consultant will ascertain rated ages from the life insurance carriers. From these analyses, you can then work with your defense team and annuity broker to develop settlement options. The guaranteed income tax free annuities that are used to fund the structured settlements add a protective layer to the plaintiff knowing that they cannotoutlive their settlement. Those options can include utilizing special needs trusts and Medicare Set Asides as further vehicles to provide for a plaintiff’s future needs at more realistic values. In the end, the goal is to demonstrate to plaintiff, utilizing all available insurance and public benefit options, how their medical care can be maximized using the amounts being offered in settlement” [ Source: CLM 2016 Orlando Florida]

The CLM piece argued in 2016 that the ACA is here to stay having survived multiple high court challenges and the longevity of insurers. [ Poignant comment.. How is that working out in late 2025?]

Impact of ACA Policy Rate Increases on Use in Settlements

I observed that settlement offers which trade the cost of future medical care for a structured settlement that pays for an ACA compliant medical insurance policy do not completely solve the problem for the following reasons:

Uncertainty of continued insurer participation in the marketplace. Several major health insurers are leaving exchanges. These include big names such as AETNA United Healthcare and Humana.

Uncertainty of cost of premiums. Without premium rate stability it is impossible to accurately fund medical insurance premiums with a structure. One will often come up short. If you have a structured settlement that pays $600 /month with a 3% COLA and then premiums go up by 10%, I asked ” where does that leave you?” Then run that deficit out 10 years or longer, perhaps to where we are today. The Milwaukee Journal Sentinel reported August 21 2016 that proposed increases could range from 5.44% to 37.88% statewide, according to filings with the federal government. In Milwaukee County, the smallest proposed increase is 9.06%. Some will be eligible for subsidies, but those ineligible for the subsidies are facing increases of 20% or more! Subsidies, in the form of credits, are available to people with incomes up to $47,520 for one person and $97,200 for a family of four. The subsidies scale back for those with incomes close to the thresholds. How about today? See Some Americans are getting sticker shock as they shop for ACA insurance, a November 3, 2025 CBC News report by Aimee Picchi “the average premium for a mid-level insurance plan surging 26% this year.

Why are premiums on ACA policies rising so much?]

The market is smaller than projected, I wrote, in 2016. The people who have bought health plans overall are sicker than predicted. And health insurers have incurred larger losses than anticipated. Health care costs continue to rise. Fast forward to 2025 and a deeper and more indelible underscore to the question of How About Now?

In my November 10, 2011 blog commentary Making a Settlement Offer in the Form of a Supplemental Needs Trust – Structured Settlements 4Real® Blog, I made the contemporaneous observation that “sometimes defendants make offers combining structured settlement and supplemental needs trust (or special needs trusts). While there is nothing inherently wrong in making an offer in this manner (the defense can make a settlement offer in whatever form it likes), and the strategy may prove beneficial on a case by case basis, the question is, can a defendant “force” a supplemental needs trust (or an ACA Plan or an HMO) on an adult plaintiff with whom the defendant is in litigation where there is good liability for the plaintiff?

Staten Island NY Obstetric malpractice case

GIVENTER v. REMENTERIA184 Misc.2d 744 (2000) 705 N.Y.S.2d 863 Full caption” EVAN GIVENTER, an Infant, by His Mother and Natural Guardian, DONNA GIVENTER, et al., Plaintiffs, v. JOSE L. REMENTERIA et al., Defendants. Supreme Court, Richmond County (February 18, 2000) .

In a medical malpractice action, the jury awarded the plaintiffs, a severely brain damaged child and his parents, a verdict of $53,735,955.The defendant doctor and hospital have petitioned this court, pursuant to CPLR 4545 (a), to reduce the amount of that award by applying collateral sources to pay for the future cost of medical care and therapies (rehabilitative services) to be received by the child.The defendants seek to apply the mother’s employee health insurance plan and the benefits received while the child is in school pursuant to the Federal Individuals with Disabilities Education Act (IDEA) to offset the financial burden placed upon the defendants by the large jury award.They also seek to have the plaintiffs enroll in a managed health care plan (HMO) where the defendants would pay the premiums.

In rejecting the HMO argument, the Giventer court reasoned that insurance which the plaintiffs do not have can never be reasonably certain to replace what the jury awarded and cannot be considered a collateral source offset.

“The defendants also suggest that the infant plaintiff can purchase his own health insurance in order to provide them with a collateral source offset. Mr. Pessalano, the defendant’s rehabilitation expert who testified at the collateral source hearing, stated that Evan Giventer could purchase insurance through Blue Cross of New Jersey for $3,000 to $3,500 per year, which after a one-year waiting period would pay out literally hundreds of thousands of dollars per year for Evan’s extensive nursing care. However, when cross-examined on this point, Mr. Pessalano’s testimony was vague and speculative. He responded that: “[i]t would pay for a significant amount” but that he could not say how much without seeing a policy. When asked if he could provide a copy of such a plan, he responded that he did not have one.

The defendants also suggest that Evan be required to become a member of a managed health care plan, an HMO. Evan currently lives at home with his family. It was never proven to this court that any insurance company would approve home nursing care as opposed to care in a residential institution. No one testified as to what level of care an insurance company would permit. The jury’s awards will permit Evan and his parents to obtain the care that they choose, from doctors and nurses of their choice, without any limitations such as preapproval or being on a list for treatment or any other constraints which accompany managed care. An HMO would not replace what the jury awarded and cannot give rise to a collateral source offset. Nor can the infant plaintiff or his guardians be required to join an HMO which may or may not accept Evan and his preexisting condition”. (Emphasis ours)

Since Giventer many questions have arisen

Have healthcare insurance policies become more liberal or more restrictive?

How restrictice are they likely to be in the future?

Is it possible to predict the increase in premiums on these policies?

What will be the impact of low interest rates on health insurers (during periods of low interest rates)

Are more companies entering the long term care insurance market, or leaving it?

There are many benefits to a Supplemental Needs Trust, but there also many restrictions and /or limitations.

A New York Defense Perspective in October 2024

“The Appellate Division, Second Department recently encountered a question of first impression regarding the interplay between the ACA and CPLR: “whether a defendant may be entitled to a collateral source hearing pursuant to CPLR 4545 for the purpose of establishing that an uninsured plaintiff’s future medical expenses will, with reasonable certainty, be covered in part by a private health insurance policy, as long as the plaintiff takes the steps necessary to procure the policy.”i

In Liciaga v. New York City Transit Authority, N.Y. Slip Op. 04257 (2d Dep’t August 21, 2024), the plaintiff sought to recover damages for injuries he sustained while conducting a track replacement project on an elevated subway line. The defendants were found negligent and the case proceeded to a trial on damages where the plaintiff was awarded, among other things, $40 million for future medical expenses. The defendants moved to set aside the verdict or, in the alternative, for a collateral source hearing on the issue of future medical expenses. The trial court denied the defendants’ motion and the defendants appealed.

Citing Nunez v. City of New York, 85 A.D.3d 885, 887¬–88 (2d Dep’t 2011… “To be entitled to a collateral source hearing, a defendant “must [merely] tender some competent evidence from available sources that the plaintiff’s economic losses may in the past have been, or may in the future be, replaced, or the plaintiff indemnified, from collateral sources.” The defendants in Liciaga argued that they were entitled to a collateral source offset because, though the plaintiff was uninsured at the time of his accident, he was eligible for insurance coverage through the ACA”.

The court relied on the plaintiff’s common law obligation to mitigate damages and the “minimum essential coverage” mandate under the ACA as further support for its conclusion.

Even if You Can Jump, there is the Question of ” How High?”

It’s not particularly credible to simply say you can buy a health insurance policy without thoughtful consideration and analysis of items such as:

1. Premiums. The ability to pay premiums however high they go. If you can’t afford the premium or lack the resources to do so that isn’t very helpful. Annual premium inflation is one issue. Mitigation through using a structure is helpful to a degree.. Premium increases generally exceed the fixed COLAs available with structured settlement annuities, Indexed linkedin options may help to a degree but there needs to be a New York admitted company that both has indexing from from the start and and does not terminate when benefits start. Pacific Life hopes to introduce a solution that may be helpful in 2026.

2. Lack of competition on pricing in many states for the most comprehensive of coverage

2. The continued availibilty of subsidies and the ability to qualify for the subsidies.

3. Coverages, Exclusions and Utilization Review

4. Benefit caps, both for certain types of treatments and aggregate5

The Senate deal allows for a December 2025 vote on whether to extend ACA subsidies The outcome will determine if Obamacare coverage remains affordable for millions of Americans.

Eastern Point Trust Company file a Dismissal Motion on November 3, 2025 in its response to the Flatirons Bank Complaint.filed on September 22, 2025.

Defendant’s Motion to Dismiss” in Flatirons Bank v. Eastern Point Trust Company, Case No. 2:25-CV-00222-KHR: Folliowing is a detailed summary of the document titled “Defendant’s Motion to Dismiss” Document 15 in the court document record.

🧾 Summary of Eastern Point Trust Company Motion to Dismiss

🏛️ Case Overview

Plaintiff: Flatirons Bank

Defendant: Eastern Point Trust Company (EPTC)

Jurisdiction: U.S. District Court for the District of Wyoming

Filing Date: November 3, 2025

Counsel for Defendant: Caleb C. Wilkins, Coal Creek Law LLC

⚖️ Grounds for Dismissal EPTC moves to dismiss the case on three primary grounds:

Improper Anticipatory Filing: Flatirons allegedly filed suit to preempt EPTC’s planned litigation in Virginia.

Lack of Personal Jurisdiction: EPTC claims no meaningful ties to Wyoming.

Failure to State a Claim: Several claims allegedly lack sufficient factual basis under Rule 12(b)(6).

🔍 Key Arguments

1. Anticipatory Filing

Flatirons filed suit shortly after an industry blog revealed EPTC’s intent to sue.

EPTC argues this was a strategic move to block litigation in Virginia, where both parties had agreed to venue and choice-of-law provisions.

Cites Black Card, LLC v. Am. Express and Buzas Baseball to support dismissal of declaratory actions filed to gain forum advantage.

2. Virginia Litigation

EPTC filed a comprehensive suit in the Eastern District of Virginia against Flatirons and 13 others, alleging:

Misappropriation of trade secrets

Racketeering

Breach of contract

Computer fraud

EPTC claims Flatirons delayed its investigation and obstructed public records access.

3. Noerr-Pennington Immunity

EPTC asserts First Amendment protection for its communications with Wyoming municipalities (Lovell and Glenrock).

Claims its cease-and-desist letters and government petitions are immune from liability under the Petition Clause.

What is the Noerr-Pennington Doctrine?

The Noerr-Pennington doctrine protects individuals and organizations from antitrust liability when they petition the government—even if their efforts have anticompetitive effects—so long as the petitioning is genuine and not a sham. Here’s a detailed breakdown of the doctrine:

🏛️ Core Principle

Noerr-Pennington immunity stems from the First Amendment right to petition the government.

It shields entities from antitrust liability when they attempt to influence legislative, executive, or judicial actions—even if the result harms competition. 📜 Origin

Named after two landmark Supreme Court cases:

Eastern Railroad Presidents Conference v. Noerr Motor Freight, Inc. (1961)

United Mine Workers v. Pennington (1965)

Further clarified in California Motor Transport Co. v. Trucking Unlimited (1972), which extended protection to all branches of government, including courts

Scope of Immunity

Covers:

Lobbying efforts

Litigation

Petitions to regulatory agencies

Even if the goal is to reduce competition, immunity applies as long as the action is a good faith attempt to influence government policy.

Sham Exception

Immunity does not apply if the petitioning is a sham—i.e., not genuinely aimed at influencing government but rather intended to harass or interfere with competitors.

Courts scrutinize whether the action was objectively baseless and subjectively intended to harm competition without a legitimate government outcome.

4. Personal Jurisdiction

EPTC is based in the U.S. Virgin Islands, with servers in Virginia.

No personnel, offices, or assets in Wyoming.

Argues that cease-and-desist letters and public statements do not establish sufficient forum contacts.

5, Failure to State a Claim

Flatirons’ complaint allegedly lacks factual specificity and relies on conclusory statements.

EPTC argues the claims do not meet the plausibility standard under Twombly and Iqbal.

🧩 Requested Relief

Primary: Dismissal of all claims.

Alternative: Stay proceedings pending resolution of Virginia litigation.

Declaration of Eastern Point’s Sam Kott Document 15-1 November 3, 2025

3. EPTC developed and maintains the intellectual property underlying the QSF 360 TM Platform, toegether with all associated servers and data in Virginia.

4. Externally, the QSF 360 TM Platform is accesible only by authorized and registered users who ahve accepted the Terms of Use built into the QSF 360TM Platform, Such terms universally contain VIrginia choice of law and venue provisions

5. EPTC’s access logs indicate that many of the Flatirons’ agents and co-conspirators named in teh Virginia I and Virginia II suits described, signed up for the QSF 360TM Platform and agreed to the Terms of Use therein.

6. Even with the requisite login credentials, an authorized user can only access the QSF 360TM platform using rgeistered , multi-factor login credentials, utilizing state of teh art industry security such as SSL and end-to-end encryption to gain access to EPTC’s Virginia -based servers and thereby the QSF 360TM platform,

7.As a separate and additional agreement, EPTC’s website contains a Terms of Use which EPTC requires users to acknowledge as a condition of accessing the website. as relevant, these Terms of Use containa conspicuously formatted forum selction clause identifying Virginia as the sole forum to hear and decide any dispute between the user and EPTC.

8. EPTC’s access logs demonstarte that agents acting on behalf of Flatirons have accessed EPTC’s webiste more than a hundred times in the relevant times leading up to this matter and have thereby acquiesced to the Terms of Use, and the associated Virginia choice of law and jurisdiction provisions, pursuant to click wrap and browse wrap.

9. The Virginia I complaint alleged that Flatirons Bank and other named defendants, conspired to misappropriate intellectual property from EPTC for the purpose of creating Flatirons Justice Escrow product. The Virginai I complaint contained a tptal of 12 causes of action and 4 named defendants.

10. On or about May 29, 2025. EPTC came into possession of additional facts and evidence which strengthened its various claims and implicated numerouos additional parties not named in Virginia 1. Shortly thereafter EPTC exercised its right under Federal Rules of Civil Procedure 41(a)(1)(A)(i) to voluntarily disiss the VIrginia 1 action without prejudice, permitting EPTC to refile the complaint with the newly discovered parties.

11.Following dismissal of Virginia 1, EPTC continued to obtain new facts that led it to believe that there yet additional co-conspirators acting in concert with Flatirons.to misappropriate EPTC’s intellectua; propety otherwise harm EPTC in violation of law. Many of these new facts were discovered indirectly through a public records act request.

13. The Virginia II complaint named 10 additional parties from those in Virginia 1. The Virginia jurisdiction was based on contractual provisions between EPTC and the various parties, the bulk of evidence being situated in the Coomonwealth of Virginia and the Defendants’ actions targeted at Virginia.

14. EPTC performed a review of available public records and determined that Flatirons Bank is a Colorado state-cartered bank registered with the Colorado Secreatry of State, with two Colorado locations, and Boulder being its primary place of business. Flatirons has no public offices in Wyoming and is not regiistered to the Secretary of State for Wyoming according to Kott’s affidavit. Upon its review, EPTC was unable to find any registration or licnesure that would eprmit Flatirons to conduct banking in the State of Wyoming, according to Kott.

Anyone familiar with our blogs, the settlement planning industry, suitability standards, and the judicial role in approving minors’ settlements will understand that an investment boasting a tempting 99.05% annualized rate of return over 13 years, coupled with an extraordinary 149.87% standard deviation during the same period*, is highly unlikely to be a suitable choice for substantial allocation for injury victims who cannot tolerate such risk. (*Backtest by Curvo.eu, for standard deviaton in USD) In statistics, the standard deviation is a measure that is used to quantify the amount of variation of a set of data values and used above as a measure of volatility.

“Analysts see more than a 90% chance the Bank of Japan will raise rates to about 0.75% during its December 18–19 meeting, marking a significant shift from decades of ultra-loose policy. Previous BoJ rate increases in March, July 2024, and January 2025 coincided with Bitcoin drops ranging from roughly 23% to 31%”.

According to Ray Dalio of the hedge fund Bridgewater Associates, it is generally not deemed suitable for significant allocation by either everyday or prominent investors. However, in 2025, Dalio revised his position, increasing it beyond the 2% allocation level he held in 2022, alongside gold. (see Ray Dalio Says 15% In Bitcoin Or Gold May Be Essential As Fiat Currencies Face Devaluation Risks July 28, 2025

Structured Settlements as a “Bridge to Crypto” a New Frontier in the Factoring Company Sales Pitch?

Says Anthony Cioppa, who runs America Annuity Funding LLC, a Boca Raton Florida factoring company “For years, we’ve helped people access their structured settlement payments early, so they could invest in real estate, launch a business, or take control of their finances. But today’s wealth-building playbook is being rewritten. With Bitcoin now embraced by institutions like BlackRock and the U.S. financial system adapting to crypto, we’ve entered a new era. Cioppa said in a press release,”Our Structured Strategy helps people reallocate capital from a slow-moving annuity into the best-performing asset class of the past decade.”

Cioppa continues “The process, which is fully compliant with all state-level Structured Settlement Protection Acts, begins with a lump-sum offer from Structured Strategy for the client’s future payments. Once the buyout is court-approved, the client receives their funds and Structured Strategy helps them navigate the process to acquire Bitcoin through an exchange or platform of their choice while the client maintains full control and ownership of their assets”.

Cioppa is a hard working guy who is very active on social media. You can see Cioppa promoting a sell structured settlements to crypto strategy on Instagram, YouTube and through press releases placed on various well known platforms..Cioppa does not appear to registered through FINRA or IAPD portals.

Increased Awareness of Legal, Structured Settlement, Settlement Planning and Judicial Communities is Sensible

I encourage each and every member of the structured settlement and settlement planning community and every trial lawyer in America to go to school on what Cioppa is promoting and decide for themselves whether such a strategy is appropriate for their particular clients’ or ward’s circumstances. Given that there are already laws on the books.

State laws already restrict investments for minors and incompetents at the time of settlement

It is unlikely that judges would approve the allocation of a minor’s or incompetent person’s settlement funds into cryptocurrency investments.

My message was made clear in prior posts. The volatility of Bitcoin and other crypto are generally not suitable for injury victims and probably would not be approved for injury victims where court approval of settlement is required.

For example, consider the New York law where New York CPLR § 1206. Disposition of proceeds of claim of infant, judicially declared incompetent or conservatee, states:

(c) the court may order that money constituting any part of the property be deposited in one or more specified insured banks or trust companies or savings banks or insured state or federal credit unions or be invested in one or more specified accounts in insured savings and loan associations, or it may order that a structured settlement agreement be executed, which shall include any settlement whose terms contain provisions for the payment of funds on an installment basis, provided that with respect to future installment payments, the court may order that each party liable for such payments shall fund such payments, in an amount necessary to assure the future payments, in the form of an annuity contract executed by a qualified insurer and approved by the superintendent of financial services pursuant to articles fifty-A and fifty-B of this chapter. The court may elect that the money be deposited in a high interest yield account such as an insured "savings certificate" or an insured "money market" account. The court may further elect to invest the money in one or more insured or guaranteed United States treasury or municipal bills, notes or bonds. This money is subject to withdrawal only upon order of the court, except that no court order shall be required to pay over to the infant who has attained the age of eighteen years all moneys so held unless the depository is in receipt of an order from a court of competent jurisdiction directing it to withhold such payment beyond the infant's eighteenth birthday. Notwithstanding the preceding sentence, the ability of an infant who has attained the age of eighteen years to accelerate the receipt of future installment payments pursuant to a structured settlement agreement shall be governed by the terms of such agreement. The reference to the age of twenty-one years in any order made pursuant to this subdivision or its predecessor, prior to September first, nineteen hundred seventy-four, directing payment to the infant without further court order when he reaches the age of twenty-one years, shall be deemed to designate the age of eighteen years; or (d) the court may order that the property be held for the use and benefit of such infant, incompetent or conservatee as provided by subdivision (d) of section 1210.

A regulatory gap exists

Structured settlement annuitants lack protections when solicited into structure settlements to cryptocurrency exchanges by unlicensed salespeople.

Consider that the annuity industry officially has secured uniformity in sales regulations across all 50 states.

The annuity sales regulation is modeled after an update from the National Association of Insurance Commissioners (NAIC).

The NAIC’s model aligns with the Securities and Exchange Commission’s Regulation Best Interest (Reg BI) requirements.

New York remains the lone outlier, but maintains a stricter annuity sales rules rooted in a fiduciary standard of care. States acted swiftly in updating their regulations to avoid federal oversight of fixed annuities by the SEC.

When it comes to structured settlements for crypto exchanges, it seems sensible that state regulators study transactions that have already occurred

How was the sale of structured settlement payment rights presented to the judge?

What was on the sellers declaration as the reason for selling? Was crypto on the declaration, so the judge could properly evaluate, as the Structured Settlement Protection Acts (in effect in all 50 states and DC) intend?

Did the seller received Independent Professional Advice? Remember the majority of states DO NOT require Independent Professional Advice.

It seems sensible that compliance departments at securities firms and financial advisory firms become aware of these types of transactions as they monitor the activities of representatives of their firms with respect to alternative assets and overall suitability requirements,

3. In a 2022 episode of the We Study Billionaires podcast, billionaire hedge fund manager Ray Dalio was asked by co-host William Green whether allocating 1% to 2% of one’s portfolio to bitcoin was reasonable. “I think that’s right,” Dalio replied. Dalio has served as co-chief investment officer of the world’s largest hedge fund, Bridgewater Associates, since 1985.Dalio is regarded as one of the greatest innovators in the finance world, having popularized many commonly used practices, such as risk parity, currency overlay, portable alpha and inflation indexed bond management.

“Upheaval in the cryptocurrency market puts teeth in a US Labor Department push to discourage retirement plans from adding digital assets to their 401(k) plan lineups. Crypto markets lost more than $270 billion just weeks after the department’s Employee Benefits Security Administration issued strongly worded guidance (CAR No. 2022-01) all but banning retirement plans from offering crypto assets.

6. On June 29, 2022 an article by Alex Hern and Dan Milmo appeared in The Guardian with the headline “Crypto crisis: how digital currencies went from boom to collapse“Savers talk of devastating losses as assets such as bitcoin and ‘stablecoins’ like terra fell sharply”

9.. The Curious Case of QuadrigaCX – Energent Media June 23, 2025 “What was at one point the leading cryptocurrency exchange in Canada, QuadrigaCX has devolved into a tangled mess of lost user funds, creditor protection initiatives, and mystery surrounding the deceased founder and missing funds. Now, QuadrigaCX is officially transitioning into bankruptcy following a ruling by the Nova Scotia Supreme Court that transfers the exchange out of the Companies’ Creditors Arrangement Act (CCAA), which it has been operating under since late January 2025″

10. If that’s not enough, on April 26, 2022, the New Jersey law firm of Console & Associates discusses data breaches related to crypto

“Over recent years, Bitcoin, Ethereum, Litecoin and other cryptocurrencies have surged in popularity and value as more and more people see the value that the asset class presents. However, hackers see the fact that everyday investors are now holding cryptocurrency as a major opportunity. In fact, over the past year, there have been several high-profile cryptocurrency hacks resulting in the loss of more than $14 billion dollars”.

11. Comedian Bill Murray loses $186,000 to hackers Bill Murray recently held an NFT auction in which most of the recouped funds were in the said wallet. The statement showed that the hacker drained 90% of the entire funds in the wallet, leaving just a little over $500 in the wake of the act. Cryptopolitan September 3, 2022

12. May 12, 2022 New York Post reports “Bitcoin’s plunge slashes the fortunes of major crypto billionaires”, the Winklevoss twins lost 40% of their respective fortunes, more than $2 Billion each at the time the story was poublished in the NY Post.. Sam Bankman-Fried, the founder and CEO of crypto exchange FTX, has lost roughly half of his on-paper fortune since March and is now worth about $11.3 billion”. Crypto billionaires losing fortunes as bitcoin tumbles (nypost.com)

13. “We’ve only scratched the surface of how bad the crypto crime wave has gotten June 13, 2022 LA Times by Matt Pearce

“These are tough days for cryptocurrency investors. Values are cratering. Prominent crypto firms are faltering. And it’s coming after a massive surge of criminal fraud that has been pummeling crypto users with unknown billions of dollars in losses with little relief in sight”

14. Bitcoin is down roughly 60% this year and some other tokens have lost even more. The ninth month of the year has historically been one of the worst for the largest cryptocurrency, falling every September since 2017. Bitcoin has averaged an 8.5% drop for the month over the past five years, according to Bespoke Investment Group”. August 31, 2022 Bloomberg

“Losses of Bitcoin Value – As the shining light of the cryptocurrency industry, Bitcoin advanced in value to a high watermark of $69,000, but the erosion of that value has declined since November of 2021. The currency currently trades roughly around the $20,000 mark a high mark in 2018 that now feels likea low mark for the worlds most well known coin. That’s almost an 80% loss in just over 6 months”.- The Crypto Updates July 12, 2022

On a $1,000,000 investment that’s a $800,000 loss. Could you handle it emotionally? What if you were not physically able to work? What if that money represented compensation for the loss of your spouse, parent or child?

17. Bitcoin Loses Steam Bitcoin is currently trading at $19,100, down 14% in the past week and down by around 4% over the past 24 hours. The world’s largest cryptocurrency is now down by a staggering 75% from its all-time high in November 2021 when its market capitalization was $1.27 trillion. It is now down to $366 billion.

Those who hung on from 2022 until now, weathering the recent pullbacks, have likely come out ahead. But if you’re considering this strategy, you’d better respect the standard deviation. It’s like riding a bull at a rodeo—how long can you hang on to that bucking bronco before it throws you off?

I’m not sure we need to keep dragging this out. Is this the kind of rollercoaster ride we want to strap a vulnerable group of investors into?

The “Bitcoin-Shitcoin” Expression

Next time someone tries to “poo-poo” the renewable credentials of Bitcoin mining, remember AmityAge Mining Farm. Founded by Gabriel Kozak and Dušan Matuska, the Bitcoin mining facility uses human and animal waste to generate electricity for mining”. According to Matuska, using renewable energies such as biogas “shows that we can really accelerate the adoption of these renewables and make their return on investment higher in the end,” while it’s also a cheap energy source. An ecologically sound and low-cost way of generating electricity, biogas electricity plants convert waste into methane gas due to a fermentation process. The gas is then burned as fuel”. Read the full story here

Structured settlement annuitants receiving stable tax exempt income shouldn’t be groomed into selling structured settlement payment rights to pennies on the dollar merchants from South Florida or Maryland to put into volatile investments with a 150% standard deviation

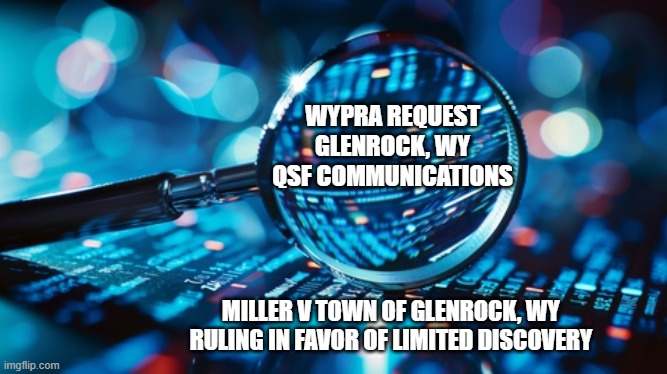

Miller v Town of Glenrock Wyoming CV 2025-0019182brings Wyoming Public Records Act compliance into focus

Court Hearingin Miller v Town of Glenrockre: WPRA

The court held a hearing on September 22, 2025, regarding Plaintiff Stephen Miller’s Motion for Preliminary Discovery, which was pending since Jul 2025.

Both parties were represented by attorneys: Caleb C. Wilkins of Cheyenne WY’s Coal Creek Law for the Plaintiff, Stephen Miller and Timothy M. Stubson of Casper WY’s Crowley Fleck PLLP, for the Defendant, Town of Glenrock, Wyoming..

“Wilkins said EPTC contacted him about one year ago with concerns its intellectual property was being stolen through a relationship between Flatirons and Lovell, Wyoming. Through a series of public records requests and the assistance of a private investigator, Wilkins said he determined such concerns had “some meat on the bone.”

While the Lovell deal fell through in February, further investigation revealed Flatirons was in talks with Evansville, Casper and Glenrock, Wilkins said. He said each of these cities were represented by Iberlin, which prompted public records requests to learn the extent of the cities’ involvement with Flatirons.

“Answers were not necessarily timely nor complete,” Wilkins said of the responses to his requests. “Even a disinterested observer could very well reach the conclusion that the [response] was intended to make it look like Glenrock was not doing business with Flatirons.”

Applicable Law Concerning Wyoming Public Records Act

The Wyoming Public Records Act provides remedies for denied access to public records.

The court must determine if the custodian’s denial of access is justified based on the law.

Court’s Decision Emphasized Need for Tranparency

The court found that Stephen Miller has standing to seek relief and that limited discovery is appropriate.

The Town of Glenrock’s argument against discovery was rejected; the court emphasized the need for transparency.

Order Details in Granted Motion for Limited Discovery

The court granted Miller’s Motion for Limited Discovery.

The Court ruled that each party may serve discovery subpoenas and is limited to five interrogatories, requests for production, and requests for admissions.

The Court furthert ruled that Discovery must be completed within 50 days, with specific limits on depositions.

Related Posts Concerning the QSF Matter between EPTC and Glenrock et al.