Structured settlements expert John Darer reviews the latest structured settlements and settlement planning information and news, and provides expert opinion and highly regarded commentary. that is spicy, Informative, irreverent and effective for over 20 years.

The STRUCTURED SETTLEMENTS 4REAL® Blog is a highly regarded source for structured settlement news, information, and commentary, led by structured settlement and settlement planning subect mater expert John Darer CLU ChFC MSSC CeFT RSP CLTC. With two decades of operation, the blog and 4structures.com are recognized as comprehensive resources, offering detailed guides and specialized insights. Established in 2005, the blog caters to a broad audience, including legal professionals, injured individuals, families, and various stakeholders, providing reviews and opinions on settlement planning. John Darer, President of 4structures.com LLC, is a seasoned structured settlement expert with over 40 years of financial services experience and 31 years specializing in structured settlements. Based in Stamford, CT, he is a Certified Financial Transitionist and Registered Settlement Planner, holding insurance licenses in 45 states and the District of Columbia. John Darer is dedicated to transparency and advocacy, he emphasizes the importance of engaging trained and licensed professionals for settlement planning, offering valuable insights through his investigative journalism and professional commentary.

A quarterly botanical‑forensic survey of the nation’s most persistent legal flora.

I. EASTERN REGION — THE ROOT SYSTEM

Henry County, Georgia

Henry County, Georgia has rekindled its civil docket Plantiff activity, to the rejoice of observers who track these blooms with the same solemnity normally reserved for the first Cherokee Rose pushing through stubborn red clay.

This is the first major Plantiff event of 2026 — not a resurgence, not a renaissance, but a rhizome remembering its purpose.

Q2 Notes:

Pure, unhybridized Plantiff spelling.

Dormant root system → active sprout.

Clerks unfazed, suggesting prior exposure.

SEO uplift measurable.

Hinds County, Mississippi

The epicenter of typographical evolution. The only known jurisdiction where the Plantiff Hedge has entered a mutational phase.

A. Plantiffus litigatorius hindsensis typica

The classic Hinds County Plantiff. Stable. Abundant. Aggressively self‑seeding.

B. Plantiffus litigatorius hindsensis mutata (The Planintiff)

The advanced mutation. Adds letters instead of losing them — a behavior botanically inconsistent with known drift models.

C. Plantiffus litigatorius hindsensis dualskiensis (The Dualski Hybrid)

The rare hybrid bloom where Plantiff and Planintiff appear in the same ecosystem. A once‑in‑a‑generation event.

Q2 Notes:

The official docket header now reads Planintiff.

Mutation fixation achieved.

No Plaintiffs detected.

Hinds County is now a monoculture.

II. WESTERN REGION — THE BLOOM CYCLE

Orange County, California (OCTLA)

The first confirmed Orange County Plantiff sighting of 2026 appears, as usual, in the OCTLA event cycle. The language shows the familiar drift — not explicitly botanical, but unmistakably chlorophyll‑adjacent — as if the organization has once again been lightly pollinated by the Jacaranda canopy.

Q2 Notes:

Floral surnames in the CLE lineup.

Pricing structures that echo the 2025 $65 Plantiff Attorney Member tier.

A general “Plant‑Advocate‑Friendly” tone.

The hedge behaves like a seasonal ornamental: it blooms annually, confuses the gardeners, and refuses pruning.

Plate OC‑1 — OCTLA Announcement Poster (2026). Evidence of anthroponymic bloom cycle in Orange County. (Satire)

The Madison Law Taproot (2024–2026)

Madison Law (Irvine, CA) remains the foundational stone of the West Coast Plantiff lineage. Though the firm has since corrected the spelling, its April 7, 2024 “Plantiff” page stands as the earliest complete fossil of the species — the taproot from which the Western hedge continues to grow.

The correction does not diminish its significance. If anything, it elevates it:

the first documented West Coast Plantiff, and

the first documented corrective event

A firm that bloomed early and then pruned responsibly is the perfect hinge between the OCTLA recurrence and the broader Western drift. It anchors the lineage, providing the geological layer that makes the Orange County bloom cycle legible.

Madison Law is not merely a historical footnote. It is the living fossil that gives the entire Western Plantiff ecosystem its root structure.

III. CENTRAL REGION — THE WANDERING TENDRILS

Central Region Dual Mutuation Event: C-2 Hashtag Bloom (National Law Review, on X.Com 3/31/26)

Because the tweet contains two independent Plantiff occurrences in the same micro‑environment:

Metadata mutation — #plantiff

Textual mutation — “plantiff” in the tweet copy itself

…it qualifies as a C‑2 Dual Mutation Event, defined as:

C‑2 — A simultaneous malaprop in both metadata (hashtags, tags, captions) and the surrounding editorial text, originating from an institutional or national‑level legal publisher.

Why this is Central Region (not Peripheral, not Deep)

It’s not Peripheral, because the host is a national legal publication, not a county clerk or boutique firm.

It’s not Deep, because the mutation is not in the article body, PDF, or legal document — only in the social‑media wrapper.

It is squarely Central, because the error appears in editorially controlled public‑facing text.

Why C‑2 matters

C‑2 events are rare and highly diagnostic:

They show parallel propagation vectors (text + metadata).

They indicate editorial breakdown, not just a stray hashtag.

They often precede T‑series incursions (full‑text “plantiff” inside the article itself).

This is the kind of event that suggests the Hedge is not just creeping — it’s testing structural weaknesses.

Taxonomic Summary

Region

Code

Description

Example

Central

C‑2

Dual mutation: metadata + text in same institutional post

National Law Review tweet, 3/31/26

This specimen fits squarely into the Central Region of the Plantiff Hedge map — the zone where:

Institutions with editorial controls

Accidentally propagate the malaprop

In metadata, headlines, or hashtags

Without the mutation appearing in the article body

It’s the region between:

Peripheral Zone — small firms, county clerks, CLE vendors

Deep Zone — full‑text “plantiff” in pleadings, orders, or published opinions

The National Law Review hashtag is a textbook Central Region incursion:

National‑level publisher

Controlled social media channel

No body‑text contamination

Public‑facing metadata error

High‑visibility propagation vector

Classification:H‑1 (Hashtag Bloom) → Central Region

Why it matters: Central Region events are the bridge species — they show the Hedge can cross from local/accidental to national/structural. They’re the ones that precede the T‑series (Textual) mutations in the same ecosystem.

2026 Major Touchstone

2026 Minor Sightings

The hedge has begun to meander, sending exploratory tendrils into the Midwest and Mountain West.

Q2 Notes:

Missouri: “Plantiff’s Mothion.”

Nevada: “Plantiff‑Forward Representation.”

Colorado: Plaintiff + Plantiff hybridization in the same sentence.

The hedge behaves like a volunteer plant: uninvited, thriving, and confusing.

IV. THE LINEAGE — 2024 TO PRESENT

2024 — The Seed

Madison Law’s “Plantiff” results page. The soil is inoculated.

2025 — The Institutional Wink

OCTLA’s $65 Plantiff Attorney Member tier. The wink becomes a nod in 2026.

2026 — The Annual Bloom

Henry County rekindles. Hinds County mutates. Orange County recurs. The hedge stabilizes.

V. STRAIGHT‑FACED SUMMARY

By Q2 2026, the Plantiff Hedge is:

Perennial in the East

Seasonal in the West

Migratory in the Central corridor

The Plantiff is no longer a typo. It is a botanical condition, a jurisdictional phenomenon, and a species of legal flora that refuses to be weeded out.

Bad faith in insurance has nothing to do with morals, manners, or how anyone spent their Sunday. It’s about insurers cutting corners — slow‑walking a claim, dodging clear liability, or refusing to settle. When that happens, the policyholder loses the protection they paid for. This article explains how bad faith structured settlements help manage exposure and resolve claims within limits.

🔹 Bad faith isn’t about virtue — it’s about conduct. When a carrier delays, denies, or deflects instead of evaluating a claim reasonably, that’s where exposure begins.

🔹 The duty is straightforward: protect the insured when liability is reasonably clear. If the insurer mishandles a settlement opportunity, the insured can be left staring at an excess verdict the carrier should have prevented.

🔹 Most bad‑faith cases aren’t born from malice — they’re born from mismanagement. Missed deadlines, incomplete investigations, low‑ball offers, or failure to respond to a policy‑limits demand can turn an ordinary claim into a seven‑figure problem.

Understanding Bad‑Faith Exposure

Insurance bad faith arises when an insurer fails to protect its insured from excess exposure by refusing to settle a claim within policy limits when liability is reasonably clear. While structured settlements rarely appear explicitly in published opinions, they are often the most effective tool for resolving the underlying disputes that create bad‑faith risk.

Bad‑faith exposure can arise in:

🔹 motor vehicle liability claims 🔹 medical malpractice disputes 🔹 commercial liability matters 🔹 professional liability cases 🔹 catastrophic injury claims 🔹 multi‑claimant accidents with limited limits

When an insurer mishandles a settlement opportunity, the insured may face a verdict far exceeding their coverage — and the insurer may be responsible for the entire excess judgment.

Why Structured Settlements Matter in Bad‑Faith Cases

Structured settlements solve problems that lump sums cannot:

In bad‑faith‑sensitive cases, these features become claims disaster‑recovery tools.

Examples of How Structured Settlements Resolve Bad‑Faith Exposure

Below are practical, visual scenarios showing how structures prevent or neutralize bad‑faith risk.

1. Clear‑Liability Auto Case With Inadequate Limits

A claimant suffers a traumatic brain injury. Liability is uncontested. The policy limit is $100,000; the life‑care plan exceeds $3 million.

A structure can:

🔹 stretch limited dollars 🔹 fund lifetime medical needs 🔹 protect the insured from excess exposure 🔹 demonstrate good‑faith claims handling

2. Commercial Liability Claim With Long‑Tail Damages

A business faces decades of projected wage loss. The claimant demands payment security.

A structure can:

🔹 match payments to future‑loss projections 🔹 reduce the present‑value cost of settlement 🔹 use funding agreements or reinsurance‑supported designs 🔹 resolve the claim before excess exposure develops

3. Catastrophic Injury Case Where the Claimant Requires Payment Security

The plaintiff refuses to settle unless future payments are guaranteed.

A structure can:

🔹 provide secure, guaranteed lifetime benefits 🔹 eliminate solvency concerns 🔹 satisfy the claimant’s long‑term needs 🔹 avoid litigation over alleged failure to settle

4. Professional Liability Claim With Disputed Future Earnings

The parties disagree on future‑loss assumptions.

A structure can:

🔹 provide indexed income streams 🔹 reduce the cost of settlement 🔹 satisfy the claimant’s need for long‑term security 🔹 avoid an excess verdict driven by future‑loss testimony

5. Employment or Wrongful‑Termination Claim With Multi‑Year Pay Exposure

A claimant seeks multi‑year wage continuation.

A structure can:

🔹 replicate salary continuation 🔹 provide tax‑efficient periodic payments 🔹 reduce upfront cost 🔹 eliminate the risk of a verdict exceeding limits

6. Multi‑Claimant Accident With Limited Limits

Several injured parties must divide a single policy limit.

A structure can:

🔹 stretch limited dollars 🔹 provide individualized payment streams 🔹 resolve all claims without triggering bad‑faith exposure

Medical Malpractice Scenario: Bad‑Faith Exposure With a Med‑Mal Insurer

Medical malpractice claims create some of the most volatile bad‑faith environments because damages are often catastrophic and juries can produce outsized verdicts.

Scenario: Missed Policy‑Limits Demand in a Birth Injury Case

A newborn suffers HIE during delivery. The life‑care plan projects $12–18 million in future medical needs. Plaintiff makes a policy‑limits demand for $1 million.

The med‑mal insurer:

🔹 delays evaluation 🔹 disputes causation 🔹 fails to respond within the demand window

The case moves toward trial. The insured OB/GYN faces catastrophic personal exposure.

How a Structure Solves the Disaster

A structured settlement becomes the only viable path to resolve the claim:

🔹 stretches limited dollars 🔹 funds lifetime medical needs 🔹 demonstrates good‑faith claims handling 🔹 protects the insured physician or hospital 🔹 satisfies the plaintiff’s need for lifetime care 🔹 prevents a catastrophic excess judgment

This is a textbook example of a structure functioning as a claims disaster‑recovery tool.

🔹 Plaintiff Recovery Trusts in Bad‑Faith Cases With Taxable Damages

Some bad‑faith cases — especially employment, commercial, or professional liability disputes — involve taxable damages such as lost earnings or front pay. When a policy‑limits demand is mishandled and the case edges toward excess‑exposure territory, both sides may need a settlement structure that provides long‑term stability without relying on tax‑free periodic payments.

A Plaintiff Recovery Trust (PRT) can serve that role in a straightforward, practical way:

🔹 manages taxable periodic payments 🔹 provides fiduciary oversight 🔹 supports budgeting and long‑term planning 🔹 helps resolve cases within limits by smoothing taxable income 🔹 demonstrates good‑faith claims handling in high‑pressure negotiations

🛡️ Disaster Recovery Planning in Bad‑Faith‑Sensitive Cases

Bad‑faith exposure is a claims disaster scenario. Structured settlements are often the most effective disaster‑recovery tool because they create settlement pathways that lump sums cannot.

Disaster Scenarios & Recovery Solutions

🔹 Policy limits inadequate → structure stretches dollars and resolves within limits 🔹 Future damages disputed → structure bridges valuation gaps 🔹 Claimant demands payment security → structure provides guaranteed future payments 🔹 Multiple claimants, one policy → structure allocates limited dollars fairly 🔹 Long‑tail commercial risk → structure transfers obligations to a carrier or reinsurer 🔹 Negotiations stall → structure creates a middle ground

Purpose:

Prevent a claims disaster from becoming a bad‑faith disaster.

Options for Structuring Settlements in Bad‑Faith‑Sensitive Cases

🔹 guaranteed payment security 🔹 lifetime medical or wage‑loss funding 🔹 protection against lump‑sum dissipation 🔹 tax‑efficient income 🔹 earlier settlement and closure 🔹 reduced trial risk 🔹 structured oversight for taxable recoveries via a PRT

Benefits for Defendants and Insurers

🔹 resolves within limits when damages exceed limits 🔹 demonstrates good‑faith claims handling 🔹 reduces present‑value cost of settlement 🔹 transfers long‑tail risk 🔹 satisfies claimant demands for security 🔹 prevents excess judgments and bad‑faith exposure

📝 Checklist: When to Consider a Structure in a Bad‑Faith Case

For Plaintiffs

🔹 need for guaranteed future payments 🔹 long‑term medical or wage‑loss needs 🔹 concern about lump‑sum dissipation 🔹 distrust of insurer solvency 🔹 desire for tax‑efficient income 🔹 need for early resolution 🔹 taxable damages requiring structured oversight (PRT)

For Defendants/Insurers

🔹 exposure exceeds policy limits 🔹 future damages disputed 🔹 need to demonstrate good‑faith handling 🔹 long‑tail risk must be transferred 🔹 multi‑claimant allocation problems 🔹 claimant requires payment security

Have a Bad‑Faith‑Sensitive Case? Let’s Talk Through the Options.

Whether you represent a plaintiff or a defendant, structured settlement tools can help manage exposure, secure long‑term obligations, and create settlement pathways that avoid unnecessary risk.

How Companies that issue Structured Settlement Annuities Rank in the Insurance Subsection of 2026 Newsweek/Statista America’s Most Trustworthy Companies Poll

3. American National (American National Insurance Company) Houston, TX

5. Mutual of Omaha (United of Omaha Life Insurance Company) Omaha, NE

6. New York Life Insurance Company New York, NY

15. Prudential (The Prudential Insurance Company of America) Newark, NJ

34. MetLife (Metropolitan Life Insurance Company, Metropolitan Tower Life Insurance Company) New York, NY

Disclaimer: Newsweek neither ranked nor expressly mentioned expressly rank structured settlement annuity issuing life insurance companies and how much structured settlements were part of the consumers’ valuation cannot be verified. Newsweek abbreviated the names/brand as consumers often do. I’ve added the names of the structured settlement annuity underwriting companies within those names for accuracy, For more clarification see source link below.

Newsweek partnered with market research firm Statista to identify America’s Most Trustworthy Companies 2026

This year’s ranking includes 700 companies in 23 industries ranging from aerospace and health care to retail and consumer goods. Rankings were determined through an independent survey of 25,000 U.S. respondents, resulting in over 100,000 evaluations that reflected the perspectives of consumers, employees and investors. The analysis also considered online media sentiment, and any company facing significant scandals or lawsuits was excluded.

Further detail about the methodology used in the Market Research by Newsweek/Statista

According to the publication…

1. Market definition: All companies headquartered in the US with a revenue over $500 million were considered in the study. Public as well as private companies were eligible.

2. Extensive survey: The core of the analysis was an independent survey of approximately 25,000 U.S. residents, who rated companies they are familiar with across the three dimensions of trust. In total, 100,000 evaluations of companies were submitted [ Watchdog note this is SIGNIFICANTLY less of a sample than the 2025 survey}. The field period ran from CW 43 to CW 45 2025).

3. Social Listening: For each company that received a sufficient number of evaluations, a Social Listening analysis was conducted. This involved researching what was said about a company, across various media segments to determine whether the public sentiment towards a company was positive, neutral or negative. In total, over 307,000 mentions were gathered. Additionally, all companies that were involved in any recent scandals or lawsuits relevant to trust were excluded from the analysis.

The overall score was composed of, 80% from the survey results, and 20% from social listening analysis. The 700 companies with the highest score have been awarded in the Newsweek /Statista survey as Most Trustworthy Companies in America 2026. The final list is categorized by industries.

I then broke out the insurers that include structured settlement annuity issuers.

Structured Settlement Consumers Should View a Variety of Sources

The Newsweek/Statista survey, which was first published in 2021, is one of several surveys and evaluations that consumers can use to help evaluate insurers prior to making decisons about structured settlements, or insurance purchases Some of the more long standing surveys, which may poll consumers, professionals and executives include:

Rating Agencies such as A.M. Best, Moodys, Standard & Poors, Weiss Ratings. Fitch and other Tier One rating agencies such as Egan Jones. Consider multiple rating agencies.

Fortune Magazine Annual Corporate Reputation survey: Life & Health Insurers section, generally published in January.

Comdex ratings. The Comdex is a composite score that ranks insurance companies by comparing their ratings from major rating agencies. Its primary purpose, like that of ratings in general, is to evaluate the financial strength of an insurance company.

Some insurers appear in multiple surveys, while other highly reputable insurers appear in only one or two. Some insurance companies that appear in the Newsweek/Statista survey do not issue structured settlement annuities.

For attorneys and settlement planners who actually know how a 468B fund is supposed to work

Treasury Regulations § 1.468B-1

The Treasury Regulations under § 1.468B-1 grant settling parties considerable latitude in structuring a qualified settlement fund. A QSF can be a state-law trust, and, in certain circumstances, if created by the defendant, it can be a segregated escrow or a bank account. The QSF Regulations are deliberately structure-agnostic.

But that latitude has been mistaken for endorsement of any contrived arrangement.

Some plaintiffs’ firms have begun to treat the absence of a categorical structural requirement as a license to run their own QSFs, with the firm itself or a single attorney within the firm controlling distributions, claim allocation, and the timing of every payment, with no independent fiduciary reviewing or having the power to exercise fiduciary powers under a properly granted license. The governmental authority claims it has “continuing jurisdiction” but does not view, approve, audit, or supervise any of the QSFs, their transactions, or the administrator’s actions. Functionally, the administrator is the lawyer, or a nominal administrator who follows the lawyer’s instructions. The QSF is, in everything but name, a mere bank account run by the plaintiffs’ counsel.

Call it what it is: a Counsel-Managed QSF

And then ask the harder question. Does it survive five minutes of Banks analysis?

The honest answer, as the law stands today, is that it likely would not.

What the QSF Regulations Actually Require

Under Treas. Reg. § 1.468B-1(c), a fund qualifies as a QSF only if it satisfies three requirements:

It must be established pursuant to an order of, or approved by, a governmental authority, and remain subject to that authority’s continuing jurisdiction.

It must exist to resolve or satisfy claims arising from a tort, breach of contract, violation of law, or one of the other enumerated bases.

It must be a trust under applicable state law, or its assets must be otherwise segregated from the assets of the transferor and related persons.

The QSF is taxed as a separate entity on its modified gross income under Treas. Reg. § 1.468B-2(a). The transferor’s payment into the QSF is generally deductible in the year of contribution (Treas. Reg. § 1.468B-3(c)). The claimants are not taxed until distribution, provided the QSF is operated as a genuine intermediary holding the funds for their eventual benefit, not as their alter ego nor under the control of the plaintiff (who is their agent).

That last clause is doing all the work.

The QSF is supposed to function like a trust, even when it is not technically organized as one. The administrator is supposed to act like a trustee, holding the assets impartially, exercising independent judgment, and making distributions in accordance with the governing documents and the directives of the supervising governmental authorities. Compare Frank Lyon Co. v. United States, 435 U.S. 561, 572-73 (1978) (formal title shifts the incidence of taxation only where the transferor has parted with meaningful control over the property).

When the administrator is not impartial, when the administrator is the agent of the claimants, and when no one with independent fiduciary discretion stands between the claimants and the cash, the QSF is functioning as a conduit. The Code does not bless conduits.

🕳️The Trustee Vacuum: Why a Law Firm Cannot Hold the Bag

Set aside, for a moment, the federal tax analysis. Start with state law.

In every state, a business entity that seeks to act as a corporate fiduciary or to exercise corporate trust powers must hold a trust company charter or an equivalent fiduciary license. The mechanism varies. In some states, the licensing authority is the banking commissioner; in others, it is the state corporation commission or a department of financial institutions. The common theme is that, where a state regulates “corporate trustees” or “trust companies,” an entity that wishes to serve as trustee of an express trust (or to advertise or hold itself out as exercising corporate fiduciary powers) may be required to be chartered or licensed to do so under that state’s statutes and regulations.

A law firm, whether organized as an LLC, PC, PLLC, LLP, general partnership, or any other entity, is typically not chartered as a trust company (this writer is unaware of any such incidence of a law firm being licensed as a trust company. Likewise, a bank, whether a state bank or a national bank, may not act in a fiduciary capacity unless it has obtained fiduciary (trust) powers under applicable banking law. Whether a particular firm or bank may lawfully serve as trustee of an express trust is a state-law and charter/authorization question and should be confirmed for the governing jurisdiction and the specific entity.

That should be the end of the conversation in any QSF that is structured as a state-law trust. It is not.

What happens in practice is that the QSF gets organized so that the individual attorney controls the QSF, or a nominal third-party administrator is engaged as an escrow agent, but the operating documents bind that administrator to follow the directions of plaintiffs’ counsel on every matter that touches the assets – from the timing of distributions, the resolution of liens, and the claim allocation among co-claimants.

Either way, the practical effect is the same. The law firm contacts a bank for an escrow account, and the lawyer runs the QSF.

And once the lawyer runs the fund, every other piece of the federal tax analysis collapses around the Banks agency principle.

Here is what the Supreme Court actually said in Commissioner v. Banks, 543 U.S. 426, 436 (2005):

The relationship between client and attorney, regardless of the variations in particular compensation agreements or the amount of skill and effort the attorney contributes, is a quintessential principal-agent relationship.

And more pointedly, on the same page:

🧑⚖️The attorney is an agent who is duty bound to act only in the interests of the principal, and so it is appropriate to treat the full amount of the recovery as income to the principal.

Banks was decided in the contingency-fee context, but the agency holding is not contingency-fee-specific. The attorney is the client’s agent because the attorney owes the client undivided loyalty and is obligated to act solely on the client’s behalf. That obligation is structural. It does not turn off because the attorney has been handed a different hat to wear in connection with the same matter.

This is the crux of the Counsel-Managed QSF problem.

A QSF requires its administrator to act independently, holding the fund’s assets impartially for the benefit of all claimants and acting under the supervising authority’s continuing jurisdiction. The attorney-as-administrator is, simultaneously, agent for one or more of the claimants and partisan advocate for those claimants’ positions in any contest over allocation, lien resolution, or distribution timing. The two roles are not merely in tension. They are categorically incompatible.

A Wood LLP analysis (Feb. 18, 2025) puts it neatly: the attorney-administrator is “wearing two hats simultaneously,” and the agency duty owed to the client makes it functionally impossible to also act with the impartiality a QSF administrator owes to the fund.

The interposition of a nominal independent administrator does not solve the problem. It often makes the problem worse. When a passive third-party administrator is bound by the QSF’s governing documents to follow plaintiffs’ counsel’s instructions, the agency conflict is actually affirmed, not eliminated. The lawyer still runs the fund. The lawyer just runs it through a willing “rubber stamp” intermediary who has no independent discretion to push back. From the IRS’s perspective, that arrangement is Hart‘s pliable trustee with a bigger letterhead.

🪢Constructive Receipt: The Pliable Trustee Test

Treasury Regulation § 1.451-2(a) sets out the constructive receipt rule:

Income although not actually reduced to a taxpayer’s possession is constructively received by him in the taxable year during which it is credited to his account, set apart for him, or otherwise made available so that he may draw upon it at any time, or so that he could have drawn upon it during the taxable year if notice of intention to withdraw had been given. However, income is not constructively received if the taxpayer’s control of its receipt is subject to substantial limitations or restrictions.

The doctrine has both a substantive arm (when must the taxpayer recognize income) and an anti-abuse arm (the taxpayer cannot turn his back on what he has the unfettered right to demand). The relevant case law for the Counsel-Managed QSF is the second arm.

Hart v. Commissioner, T.C. Memo. 1983-364, gives the canonical formulation. Constructive receipt requires “unfettered control” over the amount, directly or indirectly. Where a trustee holds funds and would remit them on the taxpayer’s demand, or where the trustee is “a pliable trustee that would accede without question to any request for funds made by” the taxpayer, the constructive-receipt doctrine applies. Where, by contrast, the trustee retains genuine discretion and the taxpayer must satisfy real conditions to obtain the funds, the doctrine does not apply.

Wolder v. Commissioner, 493 F.2d 608, 613 (2d Cir. 1974), reinforces the unfettered-command test from a different angle. An attorney-legatee did not constructively receive a bequest in 1965 because his coexecutor refused delivery and the residuary legatees objected. The Second Circuit held that “until such time as the consent of the coexecutor was obtained to the transfer, the individual taxpayer was subject to substantial limitations or restrictions.” The taxpayer’s command of the assets must be real, not nominal.

Hamilton National Bank v. Commissioner, 29 B.T.A. 63 (1933), is the original turn-his-back case. A taxpayer cannot defer income by refusing to accept a payment that has been tendered and is at his disposal. Hamilton National Bank and its progeny police taxpayers who would otherwise time their income by simply declining to take it.

Utley v. Commissioner, 906 F.2d 1033 (5th Cir. 1990), extends the same principle to controlled entities. Where the taxpayer owns and controls the obligor, he cannot avoid constructive receipt by causing the obligor to default. The taxpayer’s de facto power over the source of payment is treated as the equivalent of an unfettered right to demand.

Sidebar. When a QSF is based on an escrow account and the escrow agent has no fiduciary powers and holds no fiduciary licenses, the QSF is, by default, Counsel-Managed.

Now apply the framework to the Counsel-Managed QSF.

The plaintiff’s claim is liquidated and on deposit in the QSF. The plaintiff’s attorney, under Banks, is the plaintiff’s agent. The attorney controls the QSF, either as administrator or by directing the nominal administrator. The fund’s governing documents do not require the supervising court’s approval for distributions. There is no independent fiduciary standing between the plaintiff and the cash.

What, exactly, is the “substantial limitation or restriction” that prevents the plaintiff from demanding immediate payment? The attorney’s discretion? The attorney is the plaintiff’s agent. The nominal administrator’s discretion? The administrator is bound to follow the attorney’s instructions.

The fund is, in Hart‘s language, the pliable trustee. The plaintiff’s right to demand payment runs through the plaintiff’s own agent. That is not a substantial limitation. It is a pretend formality.

The IRS’s strongest position, on these facts, is that the claimant constructively received the QSF deposit on or near the date of funding. The structured-settlement consequences of that conclusion are not subtle. Section 130 qualified-assignment treatment is unavailable for any periodic-payment annuity funded out of a QSF whose claimant has already constructively received the underlying liquidated proceeds. The attempted structure collapses to a taxable lump sum, with the assignment company holding paper that no longer accomplishes what the parties intended.

Economic Benefit: The Irrevocable Set-Aside

The economic benefit doctrine extends beyond constructive receipt. Constructive receipt requires the taxpayer to have something he could draw on. Economic benefit reaches situations where the taxpayer could not yet draw on the asset, but the asset has been irrevocably set aside for his benefit and is no longer at the payor’s risk.

The seminal authority is Sproull v. Commissioner, 16 T.C. 244 (1951), aff’d per curiam, 194 F.2d 541 (6th Cir. 1952). An employer placed $10,500 in trust for the future benefit of its employee. The funds were to be paid out in installments two and three years later. The Tax Court held the entire $10,500 was taxable in the year of the transfer because:

the employer had irrevocably parted with the funds,

the employee had an absolute right to receive the corpus on the prescribed schedule,

the funds were beyond the reach of the employer’s general creditors, and

there were no material contingencies that could defeat the employee’s right to receive.

Compare Minor v. United States, 772 F.2d 1472 (9th Cir. 1985). Physicians’ deferred compensation was held in a trust whose sole beneficiary was the medical practice, not the physicians. The physicians had no rights greater than those of general unsecured creditors of the practice. Their interests were forfeitable. The Ninth Circuit held that the economic benefit doctrine did not apply because, as the court put it, “the employee’s interest has been [forfeitable]” and the trust assets remained at the practice’s risk.

Compare also Drysdale v. Commissioner, 277 F.2d 413 (6th Cir. 1960), where the Sixth Circuit found no economic benefit because the taxpayer’s right to the trust funds was conditional on his reaching age sixty-five, retiring from full-time activity, or his death. Substantial conditions defeat the doctrine. Pure timing rules do not.

Now run the Counsel-Managed QSF through the Sproull framework.

The defendant has paid the claim into the QSF. The defendant is no longer at risk; the funds are beyond the reach of the defendant’s creditors. The QSF holds the funds for the benefit of the named claimants. The amount is liquidated. The administrator’s discretion to withhold distributions is, in substance, the discretion of the claimants’ own agent.

What, exactly, are the “material contingencies” that protect the QSF from economic-benefit treatment? Lien resolution? Liens are typically a few percent of the recovery and do not put the entirety of the corpus at risk. Allocation among co-claimants? In a single-claimant QSF, that contingency is absent on its face. Structured settlement decisions? Those are elective. They are not contingencies that put the claimant’s right to the corpus at genuine risk.

A Counsel-Managed QSF that holds liquidated proceeds for a single claimant, with no court-approved distribution review, no independent administrator, and no genuine contingency protecting the claimant’s right to demand, looks like Sproull with a different caption. The economic benefit doctrine should reach it.

The Tax Court’s analysis in Pulsifer v. Commissioner, 64 T.C. 245 (1975), confirms the principle in the QSF-adjacent context: where funds are set aside in court for a known beneficiary, beyond the reach of the original payor’s creditors, and the beneficiary’s right to the funds is absolute, the economic benefit doctrine triggers in the year of the set-aside. A QSF held for a single claimant, with liquidated proceeds and no real contingencies, is the same fact pattern in different clothing.

What Happens If the IRS wins

The downstream consequences of a successful IRS challenge to a Counsel-Managed QSF are not minor adjustments. They cascade.

Acceleration of income. The claimant recognizes the entire QSF deposit as ordinary income (or capital, depending on the underlying claim) in the year of constructive receipt or economic benefit. Interest and underpayment penalties run from the original due date.

Loss of § 130 treatment. Periodic-payment annuities funded out of the QSF were intended to provide tax-free benefits under § 104(a)(2) and to qualify the assignment under § 130. Once the claimant has constructively received the underlying lump sum, § 130 has nothing to assign. The structured settlement collapses into a non-qualified deferred compensation arrangement, with all of the income-recognition and § 409A consequences that follow.

Carrier and exposure. The annuity issuer that took the assignment is holding paper that does not do what it was designed to do. The carrier’s expected tax treatment is upended, and the carrier may face arguments from the claimant that the structure was misrepresented. Claims professionals who built a settlement architecture on a Counsel-Managed QSF have written checks on a structure the IRS may not honor.

Settlement planner exposure. The settlement planner who recommended the Counsel-Managed QSF, prepared the structuring projection, or coordinated the funding has built professional advice on a foundation the planner should have known would not hold under the applicable doctrines. Civil exposure follows.

Counsel’s own exposure. The plaintiffs’ attorney who served as administrator, or who directed a nominal administrator, has acted in two incompatible capacities at the same time. Beyond the federal tax consequences to the client, the attorney has created professional-responsibility issues under Model Rule 1.7 (concurrent conflicts) that no engagement letter, however carefully drafted, eliminates. The agency duty Banks describes is not waivable by stipulation.

The settlement community has been told for years that QSFs are flexible. They are, but that flexibility is not unlimited. The limits are not in the QSF Regulations; they are in the doctrines that apply to every taxpayer-controlled set-aside, and they are in the agency principles the Supreme Court reaffirmed in Banks.

Practitioner Takeaways

For attorneys and settlement planners who actually have a QSF on the table, the working rules are:

🧑⚖️The administrator must be independent. Independent in fact, not just in title. An administrator who follows plaintiffs’ counsel’s instructions and lacks the fiduciary authority to reject any requests is not independent. Use a chartered institutional fiduciary or, where state law permits, an individual fiduciary who is not the claimants’ agent.

🚫A law firm cannot serve as trustee of a state-law trust QSF. State trust-company licensing requirements apply, and bank unless they have a trust charter do not satisfy them. Where the QSF is structured as a trust, the trustee must be either an individual fiduciary or a chartered trust company.

🏦An individual attorney serving as trustee creates the Banks agency conflict. The attorney’s fiduciary duty to the client is structural and continuous. ❌It does not suspend during QSF administration. The conflict is categorical, not waivable.

Court approval of distributions is a feature, not a burden. The supervising authority’s continuing jurisdiction is a regulatory requirement under § 1.468B-1(c)(1). Building genuine court oversight of distribution decisions into the QSF’s operating documents creates the substantial limitation that defeats both constructive receipt and economic benefit.

Single-claimant QSFs require special discipline. The economic benefit risk is highest where the corpus is liquidated, the recipient is identified, and the contingencies are illusory. Real allocation disputes, real lien negotiations, and real structured-settlement elections take time and create the conditions that protect the QSF’s qualification. Manufactured contingencies do not.

Document the contingencies and the discretion. The QSF’s governing documents should describe the administrator’s independent discretion, the standards for distribution approval, the supervising authority’s role, and the genuine contingencies that condition the claimants’ right to receive. Paper that recites independence while operating documents direct otherwise will not survive scrutiny.

If you would not let opposing counsel hold the settlement money in their IOLTA account pending allocation, do not let plaintiffs’ counsel hold it in a Counsel-Managed QSF. The constructive-receipt analysis on an attorney’s IOLTA is, in substance, the same analysis. The 468B label does not change it.

The Bottom Line

A QSF that is under the plaintiffs’ counsel, or that is a nominal bank acting as the administrator, is bound to follow plaintiffs’ counsel’s instructions and is a Counsel-Managed QSF. It is structurally vulnerable on two independent doctrines.

State corporate-trustee licensing requirements often restrict which entities may serve as trustees of an express trust, and a law firm entity will frequently not qualify absent a relevant fiduciary charter or license. An individual attorney may be appointable in a personal capacity under many state trust codes, but doing so can still trigger the Banks agency concern: the attorney remains the client’s agent and partisan advocate and therefore may be unable, as a practical and fiduciary matter, to serve as the independent, impartial fiduciary the QSF structure assumes.

Once the agency conflict is established, the constructive receipt doctrine (under Hart v. Commissioner and its pliable-trustee progeny) and the economic benefit doctrine (under Sproull and the irrevocable-set-aside line) reach the deposit in the year of funding. Treas. Reg. § 1.6045-5(f), Example 9 does not save the structure; it addresses Form 1099 reporting, not QSF qualification, and it describes a court-supervised class-action context that single-claimant Counsel-Managed QSFs lack.

⚠️The downstream consequences include income acceleration, loss of § 130 qualified-assignment treatment for any periodic-payment annuity funded out of the structure, civil exposure for carriers and settlement planners, and professional-responsibility exposure for counsel.

The QSF Regulations are flexible. They are not a license for plaintiffs’ counsel to run their clients’ settlement money through plaintiff counsel-controlled accounts. The doctrines that govern every other taxpayer-controlled set-aside still apply, and Banks still controls the agency analysis.

Authorities Cited

Commissioner v. Banks, 543 U.S. 426 (2005)

Frank Lyon Co. v. United States, 435 U.S. 561 (1978)

Drysdale v. Commissioner, 277 F.2d 413 (6th Cir. 1960)

Wolder v. Commissioner, 493 F.2d 608 (2d Cir. 1974)

Sproull v. Commissioner, 16 T.C. 244 (1951), aff’d per curiam, 194 F.2d 541 (6th Cir. 1952)

Minor v. United States, 772 F.2d 1472 (9th Cir. 1985)

Hamilton National Bank v. Commissioner, 29 B.T.A. 63 (1933)

Utley v. Commissioner, 906 F.2d 1033 (5th Cir. 1990)

A mailing list marketer, using the email address Todd.Edborgmarketinglist@gmail.com, has targeted NSSTA members, trying to sell them the names of people they already know—because nothing says “innovative marketing” like charging you for your own address book.

NSSTA members are going to pay to get lists of people they already know?

“From: todd.edborg <todd.edborgmarketinglist@gmail.com> Sent: Wednesday, May 6, 2026 11:28 AM To: John Subject: NSSTA B2B Email leads

Hi,

Unlock unparalleled access to key decision-makers with our exclusive National Structured Settlements Trade 2026 Industry mailing list, featuring verified emails and contact numbers.

You mustn’t miss this high-potential prospect. Kindly confirm your interest by selecting one of the following options:

• Yes, I would like to receive data insights and pricing details.

• I choose to opt out.

Regards,

Todd Edborg

VP, Business Development

Claims of “Unparalleled Access to NSSTA Members” is Baloney with Listeria

NSSTA keeps a tidy directory of its members, so paying for a bootleg copy scraped off their website is like buying sand at the beach. And if an NSSTA vendor tried to sell that info, their professional relationship would be on the express train to Awkwardville, before terminating at Kicked to the Curbsville.”

As more structured settlement designs reference external indices such as CPI‑U, the terminology used to describe them has expanded. Words like index‑linked, index‑based, and occasionally index‑backed appear in product materials and industry discussions, sometimes without clear differentiation. This brief guide provides a neutral, carrier‑friendly framework to help consumers and professionals understand what each term actually means.

🔹 Backed — The Guarantee

What it means: “Backed” refers to the financial support behind the obligation.

Structured‑settlement reality: Payments are backed by the insurer’s general account. Not by CPI‑U. Not by the S&P. Not by any index.

Why it matters: “Backed” is a solvency term. It describes who stands behind the promise, not how increases are calculated.

🔹 Based On — The Calculation

What it means: “Based on” describes the reference used to calculate increases.

Structured‑settlement reality: Increases may be based on a published index such as CPI‑U. The index informs the math, not the guarantee.

Why it matters: “Based on” is the clearest, most consumer‑friendly phrasing because it avoids implying that the index provides financial support.

🔹 Linked — The Shorthand

What it means: “Linked” is industry shorthand for “calculated using an index.”

Structured‑settlement reality: “Index‑linked” means the increase formula references an index. It does not mean the payments fluctuate with markets or that the index backs anything.

Why it matters: “Linked” is acceptable, but sometimes misunderstood by consumers as implying a deeper connection than actually exists.

Why These Distinctions Matter

These terms describe different functions, not different levels of safety:

Backed → the guarantee

Based on → the formula

Linked → the shorthand

Three different concepts. Zero overlap.

Using them precisely helps consumers understand how their payments work — without implying anything about carrier practices, product quality, or solvency.

🔹 Summary (for readers who skim)

Payments are backed by the insurer🔹.

Increases are based on the index🔹.

“Linked” is just shorthand for the calculation🔹.

Clear, consistent terminology helps everyone involved in structured settlements communicate with accuracy and confidence. Using “backed,” “based on,” and “linked” in their proper roles keeps obligations, calculations, and design features distinct, reducing the chance of misunderstanding as index‑referenced payout options continue to evolve. Maintaining this shared vocabulary supports smoother conversations across carriers, brokers, attorneys, and claims professionals, and ensures that discussions about structured settlement design remain grounded in precision.

Fast Annuity Settlement Transfers (FAST) claims that it can “help you sell your annuity”. Now the Boca Raton Florida based company.which is a multi-time Canard of the Week Winner (2024, 2025) is up for another silly ducky award. This wee\k’s nomination.

FAST’s ad copy leans hard into the friendly‑kitchen‑table trope, but the claim that it can “help you sell your annuity” is… generous. Under every state Structured Settlement Protection Act, you can’t sell a structured settlement annuity. The annuity is a “qualified funding asset” and is owned by qualified assignment company. What a factoring company like FAST can attempt to buy—subject to a court order—is your right to receive certain payments, not the annuity itself.

So when FAST positions itself as your personal annuity concierge, it’s not just imprecise. It’s structurally wrong. And in FAST’s case, it’s also on‑brand: this is the same Boca Raton outfit that has already earned multiple Canard of the Week awards for creative interpretations of basic industry terminology.

What FAST can do is petition a court to approve a discounted purchase of your future payments. What it cannot do is sell, broker, transfer, or otherwise handle the annuity contract. That distinction isn’t pedantic—it’s the entire legal framework.

Which makes FAST’s latest ad less “helpful professional guidance” and more “another duck waddling toward the podium.”

Why the Claim Is Legally Impossible

Here’s the regulator‑grade breakdown:

The annuity owner is the qualified assignment company. The payee never owns the annuity contract itself.

Payment rights ≠ annuity. A transfer involves only the right to receive certain payments.

Court approval is mandatory. No court order = no transfer. Period.

The annuity contract cannot be reassigned. Anti‑assignment clauses and state statutes prohibit it.

Factoring companies are not annuity brokers. They are purchasers of discounted payment streams, properly defined as receivables, not sellers of insurance products.

So when FAST says it can “help you sell your annuity,” it’s like a pawn shop saying it can help you “sell your bank account.” No, it can’t. It can only buy whatever you’re allowed to hand over.

FAST’s Track Record Makes the Claim Even Funnier

FAST is a multi‑time Canard of the Week winner (2024, 2025), and for good reason:

misuse of basic industry terminology

marketing that blurs legal distinctions

repeated “policy transfer” language that doesn’t exist in structured settlements

a general enthusiasm for saying things that sound good but aren’t true

This ad is simply the 2026 entry in the FAST “creative writing” series.

The Consumer‑Protection Angle

The danger isn’t just semantics. When a company tells consumers it can “sell your annuity,” it:

misrepresents the nature of the transaction

implies a level of control the consumer doesn’t have

suggests a fiduciary or advisory role that doesn’t exist

obscures the fact that the company is a counterparty, not a helper

downplays the discount rate and economic consequences

Consumers deserve clarity, not kitchen‑table stock photos and soft‑focus promises.

Bottom Line🐤➡️🦆💨

FAST can:

solicit you

offer you a discounted lump sum

petition a court

buy certain payment rights

FAST cannot:

sell your annuity

transfer your annuity

broker your annuity

change the annuity owner

modify the annuity contract

So yes — this ad earns FAST yet another nomination for Silly Ducky of the Week.🐤

At this point, the ducks are practically unionizing.

A Quick Reality Check: They Can’t Make Foie Gras Out of Your Annuity 🦆🍽️

If FAST’s marketing team wants to imply they can “help you sell your annuity,” let’s extend the metaphor to its logical conclusion: they can’t make foie gras out of your annuity any more than they can turn a structured settlement into a charcuterie board.

A secondary market annuity misnomer surfaced again downtown, in the narrow stretch between the City Café and the Metro Station. The minions were already in position—framing the page from top to bottom—as another SMA label appeared where it never belonged. It’s the kind of sighting that makes the title of this post necessary: Hersch Stern stays in bounds, but the terminology still doesn’t. That distinction—between what someone does correctly and what the terminology still gets wrong—is where the Stern–Lesk contrast begins.

Why the Stern–Lesk contrast matters in the secondary market annuity misnomer

Hersch Stern deserves professional respect. The terminology still doesn’t.

Hersch Stern remains a legitimate, established general agent in Englishtown New Jersey who actually sells annuities in the primary market. That distinction matters. It is a level of professional infrastructure, carrier relationship, and day‑to‑day annuity business that Todd Lesk never had and never operated. Stern has a real platform. Lesk had a website.

But legitimacy in the primary market does not convert factored structured settlement receivables into annuities. And in 2026, Stern is still using the same inaccurate terminology I documented in 2023 and revisited in 2025.

The quality of the receivables he moves is materially higher than the paper historically associated with Todd Lesk. That is also true. But quality does not change structure, and structure is what determines whether something is an annuity.

What Stern Is Doing Right — and What the Terminology Still Gets Wrong

🔹 Stern is a real GA with real annuity business He has carrier appointments, a functioning distribution apparatus, a primary‑market annuity practice, and real compliance infrastructure. Lesk never operated at that level.

🔹 But Stern’s SMA terminology remains inaccurate. When Stern markets “Secondary Market Annuities,” he is not selling annuities. He is selling payment rights sourced from structured settlement factoring transactions, approved under state structured settlement protection acts. The annuity contract remains owned by the qualified assignee. The investor never becomes a policyholder.

🔹 Better‑quality receivables are still receivables Stern’s inventory is generally cleaner and more conventional than the paper Lesk trafficked in. But a high‑grade receivable is still a receivable. The annuity contract never transfers. The investor never becomes a policyholder. State guaranty protections do not apply.

The Line Stern Has Never Crossed

🔹 Stern calls receivables “annuities,” but he does not take the next, far more misleading step of using insurer logos to promote them. That line matters. Once you start using insurer logos to market receivables, you have a foot in regulatory hell. Lesk did — and still does, repeatedly. Stern never has.

Using the wrong word is a terminology problem. Using insurer logos is an implied‑endorsement problem. Stern avoids the latter entirely.

2026 Context: ImmediateAnnuities Still Has the Same Inaccuracy

As of March 7, 2026, ImmediateAnnuities.com continues to publish the following:

“Secondary Market Annuities (SMAs) are policies being transferred by an annuitant pursuant to state transfer laws…”

Every material term in that sentence is wrong:

🔹 Not policies — payment rights transfer, not annuity contracts 🔹 Not by an annuitant — the transferor is a payee in a factoring transaction 🔹 Not annuities — these are factored structured settlement receivables

The persistence of this language — across Stern, Lesk, and ImmediateAnnuities — shows that the misnomer is not a fringe problem. It is structural.

Why This Matters in 2026

The market continues to present receivables as annuities, and consumers continue to assume insurer‑level protections that do not exist.

Stern deserves respect for operating a legitimate primary‑market business and for moving higher‑quality receivables. But the terminology remains inaccurate, and accuracy matters — especially when the structure of the transaction determines who the investor’s obligor actually is, what legal rights the investor does (and does not) have, what protections apply, and what risks are being assumed.

Receivables are not annuities. Not in 2023. Not in 2024. Not in 2025. And not in 2026.

Comparison Table: Stern vs. Lesk (2026)

Category

Stern

Lesk

Primary‑market annuity business

🔹 Yes — legitimate GA with carrier appointments

🔹 Once had broad FL carrier appointments, but not a GA and activity is now appears minimal

Quality of receivables

🔹 Higher‑grade, more conventional

🔹 Lower‑grade, inconsistent

Terminology (“annuity”)

🔹 Uses the misnomer

🔹 Uses the misnomer

Use of trademarked insurer logos in marketing receivables

🔹 No — never

🔹 Yes — did and still does repeatedly

Implied insurer endorsement

🔹 Avoids it

🔹 Frequently implies it

Accuracy of carrier naming

🔹 Uses the actual carrier name tied to the underlying annuity contract

🔹 Improvises carrier names, abbreviations, or hybrid labels as he goes

Ratings accuracy

🔹 Uses the actual carrier rating as published

🔹 Has made false or misleading claims about insurer ratings

Regulatory exposure

🔹 Moderate — terminology only

🔹 High — terminology + insurer‑logo use + improvised carrier naming + “Guaranteed to OutPerform” performance claim + false ratings claims

SmartAsset does a lot of good work. Their calculators, guides, and tools help millions of people understand financial decisions that would otherwise feel opaque. This post isn’t about criticizing their mission. It’s about strengthening the ecosystem they influence.

Because when a platform with SmartAsset’s reach uses terminology that insurance departments do not support, the consequences don’t stay on the page. They proliferate.

And sometimes, the irony sharpens the point. At the time of writing, SmartAsset’s homepage featured an ass in glasses under an H1 tag that read “Get Clarity.” The visual unintentionally underscores the issue: clarity begins with terminology.

🔍 The Two “Assignments” Problem — Engineered Confusion

The terminology problem isn’t cosmetic. It’s structural. Two unrelated legal mechanisms share the same word — assignment — and the industry has allowed that overlap to confuse consumers for decades.

Transfers liability to make future periodic payments.

Occurs at the time of settlement.

Moves the obligation from the defendant/insurer to a qualified assignee.

Results in the qualified assignee owning the structured settlement annuity.

The payee receives payments but does not own the annuity.

Ownership never transfers again.

This is a tax‑driven, statutory mechanism.

🔄 2. Assignment of Payment Rights (Secondary Market — Factoring)

Transfers the right to receive payments, not the obligation to make them.

Occurs years later, under state Structured Settlement Protection Acts.

Does not transfer ownership of the annuity.

Creates a receivable, not an insurance product.

Investor becomes payee‑of‑record, not annuity owner.

This is a receivables transaction.

⚠️ Why consumers get confused

Because the two assignments share a word but not a legal meaning — and then the marketplace layered “secondary market annuity” on top of that ambiguity.

The result is predictable: consumers and advisors think they’re buying an annuity. They aren’t.

📊 Clarity Table: What These Products Are vs. What They’re Called

To cut through the terminology drift, here is the distinction that matters.

Term

Accurate?

Regulatory Position

What It Actually Is

Notes

Structured Settlement Annuity

✔️ Yes

Issued by a licensed insurer; after a qualified assignment under IRC §130, owned by a qualified assignee

Insurance contract funding periodic payments

Payee is the beneficiary, not the owner. Ownership does not transfer in factoring (NAIC).

Structured Settlement Payment Rights

✔️ Yes

Transfer governed by state SSPAs

A stream of payments assigned via court order

This is what investors actually receive.

Receivable / Assigned Payment Stream

✔️ Yes

Treated as a receivable; not regulated as insurance

A right to receive payments from an insurer, dependent on a third‑party servicer

Requires ongoing servicing. The SuttonPark servicing collapse is a recent, extreme example of what can go wrong when servicing fails — delayed payments, misapplied funds, and investor uncertainty. No statutory insurance protections apply.

Secondary Market Annuity (SMA)

❌ Misnomer

Not recognized as an annuity under insurance law

Marketing term for factored payment rights

Proliferates confusion; rejected by regulators.

In‑Force Annuity Purchase

❌ Incorrect

Ownership of the annuity cannot be transferred

Not an annuity purchase

NAIC: the annuity stays with the qualified assignee.

🧩 Servicing Risk: The Part Almost Nobody Tells Consumers

Servicing risk is the part of the receivable that consumers never see in the marketing — and the part the industry has consistently downplayed. I’ve been writing about this risk since 2009 because it is structural, not theoretical. When you buy a receivable, you are relying on a servicing company to administer, track, and route payments correctly. That link is invisible to consumers, but it is essential to the product.

The SuttonPark servicing collapse was a recent, extreme illustration of what happens when that link breaks:

delayed payments

misapplied funds

investor confusion

annuitant confusion

no insurer‑backed protections

None of this risk exists with an annuity — because investors do not own the annuity. They own a receivable that depends on a servicer. And when the servicer fails, the investor feels it immediately.

This is why terminology matters. This is why clarity matters. And this is why mislabeling a receivable as an annuity misleads the very people trying to understand the risk.

🎯 SmartAsset Cannot Misinform Advisors or Investors

SmartAsset’s core audience is investment advisors and investors — people who rely on the platform for clarity, not marketing gloss. That creates a duty of accuracy. A platform that positions itself as a trusted guide cannot misinform advisors or investors by using terminology that insurance departments do not support.

When a receivable is described as an annuity, the risk profile is misrepresented. Advisors make recommendations based on that language. Investors make decisions based on that language. And SmartAsset’s credibility depends on getting that language right.

The SuttonPark collapse was a real‑time reminder that receivables carry servicing risk — a risk that does not exist with annuities. Omitting that distinction does a disservice to the very audience SmartAsset is trying to help.

📚 Wikipedia Shows the Drift in Real Time

Even Wikipedia illustrates the tension. The entry repeats the industry’s legacy phrasing — “secondary market annuity” — and then immediately acknowledges that the term is a misnomer under insurance law.

The coexistence of bad terminology and the correction of that terminology in the same paragraph shows how deeply the confusion has taken root.

This isn’t opinion. It’s documentation.

🔗 The Lead‑Generation Pathway and the Risk of Amplification

SmartAsset operates a large‑scale lead‑generation platform. If advisors sourced through that platform steer investors into factored structured‑settlement payment rights described as “annuities,” then SmartAsset is indirectly amplifying the proliferation of bad terminology.

Are you better off selling life‑contingent structured settlement payments for pennies on the dollar, or keeping guaranteed lifetime, tax‑free payments? The post’s answer is unequivocal: keeping them is almost always the better financial outcome.

2. The “Bad Idea” Being Critiqued

A new secondary‑market entrant claimed:

“You don’t know where you’ll be in 5 years and if you die the payment goes away. Selling off your payments… is a much smarter idea.”

This is entirely illogical and preadatory

Payments can be direct‑deposited anywhere, so “you don’t know where you’ll be” is a meaningless scare tactic.

Life‑contingent payments are valuable precisely because you may outlive mortality tables.

Selling eliminates the upside and locks in a deep discount

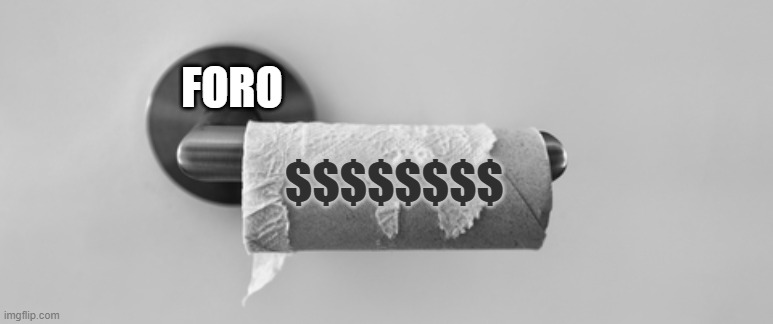

3. FORO: Fear of Running Out

The post identifies FORO as the emotional lever used to push sellers into bad deals. Darer reframes it:

Lifetime payments protect you if you live to 75, 80, 90, 100+.

A local assisted‑living facility has a 103‑year‑old resident — a reminder that longevity risk is real and valuable.

4. Why Life‑Contingent Sales Are Especially Bad Deals

The buyer must:

Purchase life insurance on the seller (often someone with impaired mortality).Unhedged deals have a deeper a deeper discount.

Price in the risk of heir disputes after the seller’s death.

Only pursue large deals, because small ones don’t make economic sense for them.

Average transactions are around $45,000, and only “big deals” work for buyers.

5. Practical Realities

Changing address or bank account is simple — the annuity issuer just needs updated information. This dismantles the “you don’t know where you’ll be” argument.

6. Consumer Protection Warning

It is prudent for payees to take their time and seek guidance from verified, credentialed professionals.

CSSC, MSSC, RSP, CFP, CLU, ChFC, CPA.

Warns that some secondary‑market content is written by people with little financial education or falsified credentials.

Alerts parents: if someone calls claiming to be “from the courts” about a child’s settlement, hang up — it’s spoofing.

7. Author’s Position (Grounded)

Selling life‑contingent payments is rarely in the seller’s best interest.

The marketing pitch is fear‑based, misleading, and financially illiterate.

Lifetime income is a critical safety net, especially for injured individuals